William Lyon Homes (NYSE: WLH) on Thursday reported net income of $8.1 million for its first quarter ended March 31, 2019, or $0.21 per diluted share, compared to $8.3 million, or $0.21 per diluted share in the prior year. The results beat analyst expectations by a penny per share.

Among the results:

- Pre-tax income of $20.0 million, up from $15.4 million in the prior year

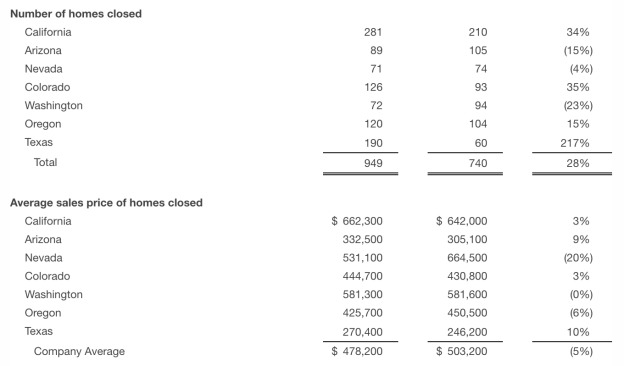

- New home deliveries of 949 homes, up 28%

- Home sales revenue of $453.8 million, up 22%

- Average sales price (ASP) of new homes delivered of $478,200 versus $503,200

- Home building gross margin percentage of 16.0%

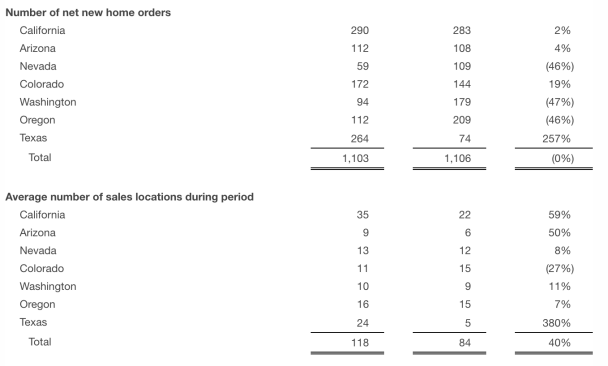

- Net new home orders of 1,103

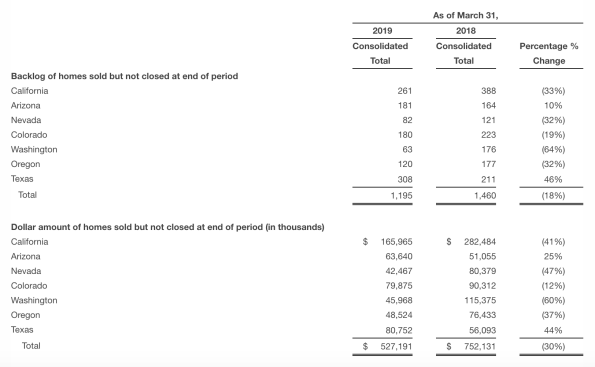

- Units in backlog of 1,195

- Dollar value of homes in backlog of $527.2 million

- SG&A percentage of 12.0%, compared to 12.7%

- Adjusted EBITDA of $36.6 million

- Average sales locations of 118

Home sales revenue for the first quarter of 2019 was $453.8 million, as compared to $372.4 million in the year-ago period, an increase of 22%. The increase was driven by a 28% increase in deliveries to 949 homes, compared to 740 in the first quarter of 2018, partially offset by a 5% year-over-year decline in the average sales price of homes closed. The decrease in ASP is based on a change in product mix with a higher concentration of deliveries from Texas.

Home building gross margin percentage for homes closed during the first quarter of 2019 was 16.0%, compared to 17.5% in the prior year period. The year-over-year decrease was primarily attributable to higher sales incentives on homes closed during the first quarter. Incentives as a percentage of revenue was 3.3% during the first quarter of 2019 as compared to 2.1% during the first quarter of 2018.

Net new home orders for the quarter were 1,103, in line with 1,106 in the first quarter of 2018. Net new home orders reflect a decrease in sales pace, as community count increased to 118 average sales locations, from 84 in the year-ago period, an increase of 40%. Our cancellation rate for the first quarter of 2019 was 16%, which is higher than the 10% experienced in the first quarter of last year, but down significantly from the 24% cancellation rate we experienced during the fourth quarter of 2018.

Sales and marketing expense during the first quarter of 2019 decreased to 5.6% of home building revenue, compared to 6.1% in the year-ago quarter, primarily due to a decrease in advertising and model operations expense during the quarter. General and administrative expenses decreased to 6.4% of home building revenue, compared to 6.6% in the year-ago quarter, primarily due to improved operating leverage.

Pre-tax income was up 30.0% to $20.0 million, from $15.4 million in the prior year. Provision for income tax was up to $4.9 million, for an effective tax rate of 24.4%, compared to a provision of $2.8 million, or 18.3%, in the prior year. The increase is attributable to certain one-time discreet items regarding stock compensation expense during the current year.

Net income attributable to non-controlling interest was $7.0 million during the first quarter, which was higher than our prior expectations due primarily to the timing of an additional phase of deliveries in a joint venture project in Southern California.

At quarter end, cash and cash equivalents totaled $45.7 million, owned real estate inventories totaled $2.3 billion, total assets were $2.9 billion and total equity was $1.0 billion. Total debt to book capitalization was 57.4%, and net debt to net book capitalization was 56.6% at March 31, 2019, compared to 56.6% and 55.9% at December 31, 2018, respectively.

On May 1, 2019, the Board of Directors of the company approved a limited waiver at the request of William H. Lyon solely for purposes of Section 203 of the Delaware General Corporation Law to allow Mr. Lyon and certain of his affiliates (the “Lyon Stockholders”) to enter into certain arrangements with potential unaffiliated co-investors in connection with potentially making a proposal for a possible business combination with the Company, as described in more detail in the Schedule 13D amendment filed by the Lyon Stockholders on the SEC’s website on May 2, 2019. Mr. Lyon has indicated that he is not engaged in active discussions, the company is not aware of any imminent proposal, and there is no assurance that granting this waiver will lead to any potential transaction.

“The first quarter of 2019 played out generally as we expected, and reflected a nice rebound from the volatility experienced late last year, as interest rates have receded and consumer demand has rebounded against a backdrop of ongoing strength in the broader economy,” said Matthew R. Zaist, president and CEO. “One of our objectives coming into the year was to deliver on our spec inventory, and our operating teams performed well in converting these homes to sell and close during the quarter. This represented 41% of our deliveries for the quarter, highlighting the attractiveness to the entry-level consumer of inventory available to the needs-based buyer.”

“Overall our backlog conversion rate was 91% for the quarter, the highest in several years, and yielding 949 new home deliveries, an increase of 28%, and home building revenues of $453.8 million, up 22% over the prior year. In addition, we had significant improvement in pre-tax income of 30% year-over-year, and SG&A leverage was better than our expectations by 100 basis points.”

Zaist continued, “Net new home orders for the first quarter were flat compared to last year’s very strong first quarter, and the order cadence accelerated each month as the quarter progressed. Our monthly order pace was 2.4 sales per community in January, improving to 2.9 in February, and picking up meaningfully in March to 4.1, bringing us back in line with historical norms. We continue to benefit from our strategy of focusing on the entry-level and first-time move-up buyer segments, which represent 83% of our deliveries and our ending backlog, and the highest absorbing segments for the Company during the quarter.”