The New Home Company Inc., Aliso Viejo, California (NYSE: NWHM) on Tuesday reported net income of $1.6 million, or $0.08 per diluted share, for the 2019 second quarter ended June 30. T The gain compared to $0.1 million, or $0.01 per diluted share, for the 2018 second quarter. Analysts were looking for a gain of $0.02 per share.

The company also announced Tuesday that Larry Webb will become executive chairman effective August 30, 2019 and that current president and COO Leonard S. Miller will become president and CEO. Miller, 56, joined the company as COO in 2017 and was appointed president in January 2019. Prior to NEW HOME, Mr. Miller worked at Richmond American Homes where he had regional and divisional responsibility for several markets in the western United States. Miller earned a Bachelor of Science degree from the University of Southern California in Accounting and a Masters in Business Administration from San Diego State University.

Total revenues for the 2019 second quarter were $162.7 million compared to $155.6 million in the prior year period. The year-over-year increase in net income was primarily attributable to a 20% increase in home building revenue, a 200 basis point improvement in our SG&A rate, a $0.3 million increase in joint venture income and a $0.6 million gain on early extinguishment of debt. These items were partially offset by a 50 basis point decline in home sales gross margins and a lower fee building gross margin due to lower fee construction activity.

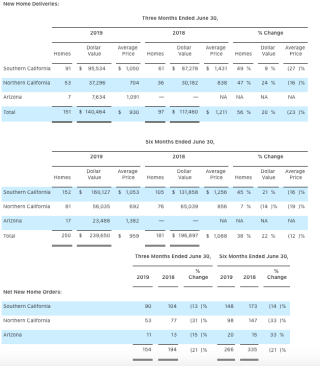

Wholly Owned Projects home sales revenue for the 2019 second quarter increased 20% to $140.5 million, compared to $117.5 million in the prior year period. The increase in home sales revenues was driven by a 56% increase in deliveries, partially offset by a 23% decrease in average selling price to $930,000 from $1.2 million a year ago. The lower year-over-year average selling price was impacted by mix, particularly in Southern California, where the 2018 second quarter included deliveries from several higher-priced, closed-out communities in Orange County.

Gross margin from home sales for the 2019 second quarter was 12.1% as compared to 12.6% in the prior year period. The 50 basis point decrease was primarily due to higher interest costs and incentives, which were partially offset by a product mix shift. Adjusted home building gross margin, which excludes interest in cost of home sales, was 16.5%* for the 2019 second quarter, compared to 15.8%* in the prior year period. The SG&A expense ratio was 11.1% versus 13.1% in the prior year period. The 200 basis point decrease in the SG&A rate was primarily due to improved leverage from higher home sales revenue, reduced marketing and advertising spend as compared to last year and to a lesser extent, lower personnel expenses. These decreases were partially offset by higher amortization of capitalized selling and marketing costs.

Net new home orders for the 2019 second quarter decreased 21% to 154 homes due to a slower monthly sales absorption rate, partially offset by an increase in average selling communities. The monthly sales absorption rate for the company was 2.4 for the 2019 second quarter compared to 3.2 for the prior year period. Due to community closeouts late in the 2019 second quarter, NWHM ended both the 2019 and 2018 second quarters with 20 active communities.

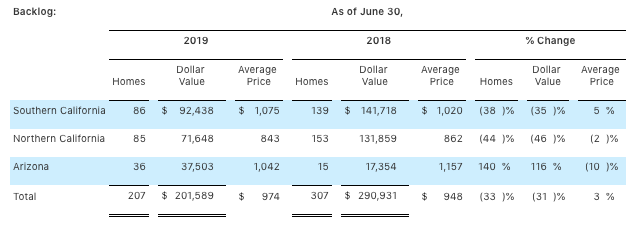

The dollar value of the company’s wholly owned backlog at the end of the 2019 second quarter was $201.6 million and totaled 207 homes compared to $290.9 million and 307 homes in the prior year period. The decrease in backlog units and value was driven by a higher backlog conversion rate for the 2019 second quarter coupled with a 25% decline in the monthly sales absorption rate. The backlog conversion rate was 74% and 46%, respectively, for the 2019 and 2018 second quarters.

The increase in the 2019 conversion rate resulted from the company’s move to more affordably priced product, which generally has quicker build cycles, as well as the company’s success in selling and delivering a higher number of spec homes.

Fee Building Projects Fee building revenue for the 2019 second quarter was $22.3 million, compared to $38.1 million in the prior year period. The decrease in fee revenues was largely due to less construction activity in Irvine, California due to lower demand levels in that submarket. Additionally, management fees from joint ventures and construction management fees from third parties, which are included in fee building revenue, decreased to $1.1 million for the 2019 second quarter as compared to $1.4 million for the 2018 second quarter. The lower fee building revenue and decrease in management fees resulted in a fee building gross margin of $0.5 million for the 2019 second quarter versus $1.1 million in the prior year period.

The company’s share of joint venture income for the 2019 second quarter was $0.2 million as compared to a loss of $0.1 million in the prior year period, with the majority of the income generated from the company’s Mountain Shadows luxury community in Paradise Valley, Arizona. At the end of 2019 and 2018 second quarters, joint ventures had six and seven actively selling communities, respectively.

As of June 30, 2019, the company had real estate inventories totaling $542.0 million and owned or controlled 2,784 lots through its wholly owned operations (excluding fee building and joint venture lots), of which 1,180 lots, or 42%, were controlled through option contracts. The company ended the 2019 second quarter with $48.2 million in cash and cash equivalents and $375.1 million in debt, of which $66.0 million was outstanding under its revolving credit facility. At June 30, 2019, the company had a debt-to-capital ratio of 61.1% and a net debt-to-capital ratio of 57.7%.

The company’s current estimate for the 2019 third quarter:

- Home sales revenue of $100 – $120 million

- Fee building revenue of $10 – $15 million

- Home sales gross margin of 12.0% – 12.5%

The company’s current estimate for full year guidance for 2019 is as follows:

- Home sales revenue of $480 – $510 million

- Fee building revenue of $65 – $75 million

- Home sales gross margin of 12.0% – 12.5%

“I am very pleased with our second quarter results which included both top and bottom-line growth while making significant progress towards reducing our leverage and strengthening our balance sheet,” said Larry Webb, chairman and outgoing CEO of The New Home Company. “Home sales revenue increased 20% year-over-year from 56% more home deliveries, and our pretax income was up meaningfully over the prior year. In addition, we repurchased $7.0 million of senior notes during the quarter which, when combined with a net $18 million pay down of our revolving credit facility, resulted in a 240 basis point sequential decrease in our net debt-to-capital ratio to 57.7%*.” Mr. Webb continued, “We experienced solid sequential improvement in our sales absorption pace across all markets, with the 2019 second quarter monthly absorption rate of 2.4 sales per community up 41% over the 2019 first quarter, resulting in a 38% sequential increase in net new orders. We also continued to recognize benefits from our strategic repositioning to more affordable product as sales from these communities represented a higher proportion of our 2019 second quarter net new orders, as well as a higher sales absorption pace than our companywide average.” Mr. Webb concluded, “We remain committed to the initiatives established earlier this year to maintain a lower cost structure, strengthen our balance sheet and generate long-term value for our shareholders. I am proud of the progress we’ve made to date and we will continue to focus on these initiatives to further position the company for long-term success.”