More than the generations before them, today’s young consumers struggle to achieve the American dream of homeownership. Escalating home prices, stagnant wages, and modestly increasing mortgage rates are contributing to a decline in housing affordability that is expected to continue this year. The National Association of Realtor’s Housing Affordability Index, which measures whether a median-income family earns enough to qualify for a loan on a median-priced home, has fallen over 20 points to 144.0 in the past three years. Lower index readings indicate worse affordability.

In addition to these barriers to ownership, many first-time buyers avoid looking for a new home because they are confused or overwhelmed by the process, especially when it comes to down payments and financing. Recent studies show that these crucial elements of the home-buying equation are laden with misconceptions and outright myths, starting with how much money is needed upfront. According to the Urban Institute, nearly 65% of renters 40 years old or younger believe they need to put down 15% in order to buy a home, even though the national median down payment for first-time buyers is 5% to 7%.

In addition, one in four Americans 35 years old or younger believe they need to have a perfect credit score to be considered for a mortgage. However, online loan marketplace LendingTree indicates the minimum credit score for a conventional bank mortgage is 620, which is considered average on the FICO credit score model that ranges from a low of 300 to a high of 850.

This confusion is impacting the number of houses sold in the U.S. Across the country, these financing falsehoods are keeping millions of would-be buyers out of sales offices and model homes. As many as 19 million Americans aged 40 or younger have credit profiles and income that are strong enough to qualify for a mortgage but choose to rent instead, according to the Urban Institute.

This means builders who cater to entry-level buyers have an opportunity to significantly expand their sales by helping these buyers better understand financing basics. The outreach should start with making the numbers easier to digest, says Mollie Elkman, CEO and president of Philadelphia-based Group Two Advertising, a home builder marketing agency that helps connect clients to qualified home buyers.

“It’s always helpful to calculate monthly payments for buyers if you are able to,” Elkman says. “Seeing the home price easily scares people away, while seeing what it looks like month-to-month like they are used to [with other payments] can pull them in.”

Zillow

Fredericksburg, Va.–based Atlantic Builders says it has experienced success reaching first-time home buyers by placing mortgage calculators on its website. Additionally, many builders offer free education sessions about homeownership and work closely with preferred lenders to aid first-time homeowners through the search process. Evans, Ga.–based Ivey Homes holds a series of finance-focused events where preferred lenders discuss financing with potential buyers. The builder says such events help drive traffic and educate buyers. Ivey Homes also educates its sales team about financing, to ensure that associates have confidence about the subject when talking to customers.

Many building firms that cater to young customers have sections on their websites dedicated to clarifying the home-buying process. For instance, big builder Lennar provides resources and best practices for first-time buyers. South Carolina-based SK Builders’ site helps first-time buyers understand what they can afford, whether they qualify for a mortgage, and how to look at factors related to mortgage qualification.

While buyers appreciate information that can help smooth their financing decisions, Elkman cautions against taking the education piece too far. “Builders understand that the first-time buyer needs more in the buying process. [However], many companies think this can be accomplished by attempting to hand-hold the buyer,” Elkman says. “No buyer wants to be babied or treated like they don’t know what they’re doing.”

Instead, Elkman explains that first-time buyers readily respond to information that fosters trust with a builder at each touchpoint. The information could be as simple as prices, images of homes built, and details about available homes. Elkman says it used to be common practice for builders to withhold such information in attempts to get people to register for their websites. Such practices are now outdated and can hurt builders, Elkman notes. Giving buyers the information they need to make decisions can establish trust from the very beginning of their home search.

Get Smart

An emphasis on technology is particularly important when attempting to reach first-time millennial buyers, says Debra Still, CEO and president of Pulte Financial Services, which provides lending services to millions of homeowners and finances new-construction homes for Pulte Homes, Centex, Del Webb, DiVosta, and John Weiland Homes customers. Digital marketing can be one of the most effective ways to reach renters who are unaware they are eligible to qualify for a mortgage.

For instance, Elkman counsels home builder clients to target consumers with specific IP addresses at apartment buildings to guarantee reaching young renters. She says demographic and behavioral information is tracked online and can be used by marketers to develop a mailing list for the exact age group builders are looking to target. Such IP address targeting is a paid digital tactic, so builders looking to employ this strategy would need to work with a third party, such as a marketing firm.

According to Still, one marketing message that resonates with buyers of all ages has to do with the financial advantages of buying new construction. New-home builders should consider offering to pay closing costs or provide lower interest rate mortgages—practices that are atypical when buying an existing property, Still says. Communicating this with potential homeowners can go a long way toward helping more first-time buyers consider new-construction homes.

What Savings?

While many young Americans have false notions about what it takes to buy a home, one distressing fact about this demographic can’t be denied: Many of them haven’t saved a penny toward a new home.

According to Apartment List, almost half of millennial renters have no down payment savings, and only 11% have saved $10,000 or more. In fact, two-thirds of millennial renters would require at least two

decades to save enough for a 20% down payment on a median-priced condo. The prolonged saving time further delays potential first-time home buyers while also discouraging younger buyers who are now much older than their parents were when they bought their first home.

The share of median income needed for a 20% down payment on a median-priced home was 23.3%, compared with 18% just six years ago, according to the Urban Institute.

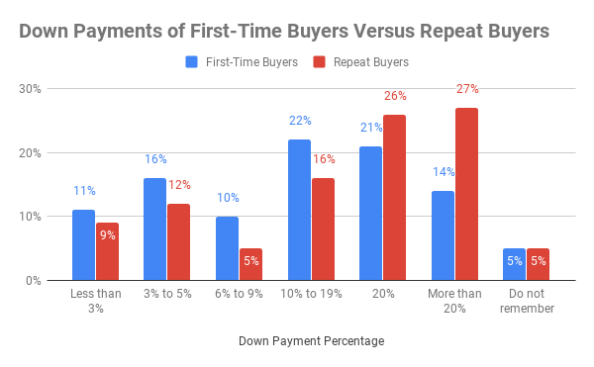

When new buyers make their first purchase, many are financially unable to afford the down payment by themselves. A Zillow report shows that half of first-time buyers rely on two or more sources for their down payment, compared with 37% for repeat home buyers. The report also found that first-time buyers were more than twice as likely to receive help from family and friends than repeat buyers, and among first-time buyers, gifts accounted for nearly one-quarter of total down payment costs.

Additionally, many millennials—often referred to as the renting generation—have prioritized education and delayed marrying and having children, key triggers associated with buying a home. As a result, the median age for first-time millennial home buyers is nearly 30 years old, according to research from mortgage service provider Ellie Mae. When they do buy a home, 32% of first-time buyers put 6% to 19% down, while 16% put 3% to 5% down, Zillow found.

“The main challenge we’re seeing for first-time home buyers is that they don’t have equity in a current home that they’re selling to use for cash for the down payment [toward another home],” says Tracey Shell, vice president for Atlanta-based Down Payment Resource. “That’s why you see the down payment hurdle still remaining … in the minds of most first-time home buyers.”

On the Rise

The good news, says NAHB chief economist Robert Dietz, is that new-construction starts are on the upswing for many first-time home buyers, suggesting there are areas for growth with the first-time buyer market share. Additionally, Dietz says townhouse construction has increased 24% in the past four quarters compared with the previous four, which could offer more opportunities for first-time buyers to purchase a new home.

Despite declining affordability in many markets and down payment misconceptions, the national homeownership rate for those younger than 35 years old reached 38.6% in the third quarter of 2018, the highest level since 2013. As more young Americans enter the home-buying arena, builders will need to be prepared to shepherd them through the process.

“For this first-time home buyer generation, marrying the personal touch and the personal relationship with technology is the way to think about outreach to these consumers,” Still says.