1

of 7

Michele Gale would prefer that people don’t know that her family rents the home where they have lived for nine years.

“I find it very embarrassing that we have been married for 17 years, and we don’t own a home. It’s sometimes hard to sleep at night thinking that we have paid them $130,000 of our money to pay for somebody else’s house. … It’s a bitter pill to swallow. I don’t feel successful.”

The fact that her husband is a lawyer, a profession that people automatically assume equals success, makes the embarrassment that much keener for the 39-year-old, stay-at-home mother who homeschools three daughters.

Still, she is grateful because if it had not been for a last-minute case of cold feet, her family would be in worse shape, among the ranks of people who lost their homes to foreclosure. During the peak of the housing boom a Realtor convinced the family that they could afford to buy a home with an interest rate that would be low at first and then increase in two years, nearly doubling the mortgage payment.

“The Realtor was so sure that we would be able to refinance the house in two years, but it just didn’t feel right,” Gale says. So the family backed out of the deal at the last minute. She believes the family dodged a bullet because the house lost value and they would not have been able to refinance the loan.

“We would be out on the street right now if we had signed that paper,” Gale says. “It would have been foreclosed on.”

— T.B.

As a freelance real estate photographer working his way through college, John had a bird’s eye view of the housing boom. “Four years ago I wouldn’t have bought a house even if I had been in a position to buy one. Everything was really expensive.”

Now, however, the only thing preventing John (not his real name) from buying a home is a more permanent job. Still working as a part-time photographer, among other odd jobs, he notes that Seattle has turned into a buyer’s market. “If I could get a full-time job with a decent salary, I’d buy a house.”

Our nationwide “Housing 360: Insights into Homeownership” survey of more than 3,000 Americans, coupled with six focus groups, indicates that a big slice of the population is in the same boat. Lots of people would be buying homes right now, if they had steady work, enough savings for a down payment, and/or a cleaner credit record. But that’s asking a lot in an economy marked by high unemployment, depletion of net worth, and tighter underwriting standards.

Seven out of 10 people responding to our survey said it’s a very good time to buy a home. They see that home prices have declined, mortgages are cheap, and lots of bargains are available. But many people don’t have the money, the credit, or the inclination to go out and participate in what could be the housing market of a lifetime.

Our focus groups turned up many people who bought a home during the boom who wish they hadn’t. “I’m angry because I own a home now and we are upside down,” said one San Diego focus group participant, speaking for the 25 percent of our survey respondents who owe more on their home than it’s worth. “Back in 2006, I should have stayed renting. I bought at completely the wrong time.”

The focus groups turned up a ton of resentment toward banks and brokers who convinced people to buy more house than they really needed or could afford. They also unearthed a lot of hostility toward greedy friends and neighbors who bought more home than they could afford, or who kept borrowing against their home as it escalated in value, then brought down values in the whole neighborhood with a foreclosure.

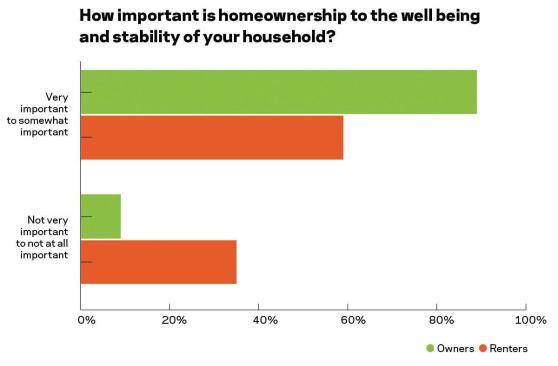

Americans have a conflicted view toward housing today, to be sure. The survey findings show that a full 72 percent of the country still believes that owning a home is an important part of their family’s dream and the American economy. And in our focus groups most people concurred that achieving homeownership says something about a family’s success and stability.

Acting on the dream of homeownership in today’s economy is where the results get sobering. Our quantitative survey turned up remarkable apathy toward making a move. “A lot of people out there are shellshocked and waiting,” says Kent Colton, the former executive officer of the NAHB whose Colton Group conducted the report for Hanley Wood, LLC, publisher of Builder. “Their sense of urgency is gone. They are just waiting.”

Here are the major takeaways from the survey and focus groups:

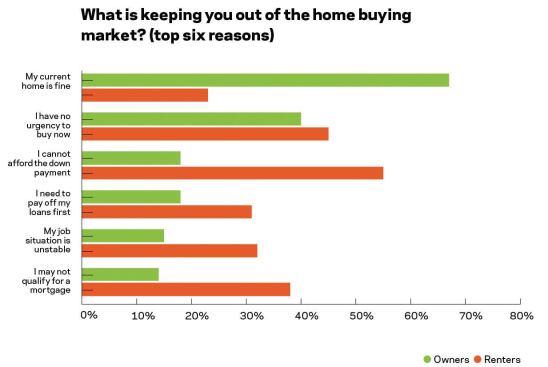

Americans feel significant apathy toward moving today. When we asked people why they weren’t buying, the top response was “My current home is fine,” cited by 67 percent, followed by “I have no urgency to buy now,” checked by 40 percent. No wonder the trade-up housing market remains in the dumps: People are content to stay put until the storm clears.

Many households would like to recover some of their lost paper equity before they move on. Nearly half the survey respondents (47 percent) expressed concern about selling their current home for a fair price. And since a quarter of the household population is underwater on their homes, they would have to write the bank a check at closing.

Renters are much less satisfied with where they currently live—only 25 percent say their current home is fine. But 45 percent said they have no urgency to buy either. Why don’t they move? The top reason was that they don’t have the money for a down payment (55 percent), and they are afraid they won’t qualify for a mortgage (38 percent). Also, about one-third of renters said they would have to pay off other loans and land better jobs before they would move.

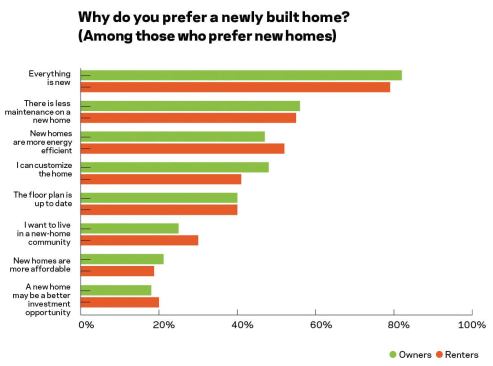

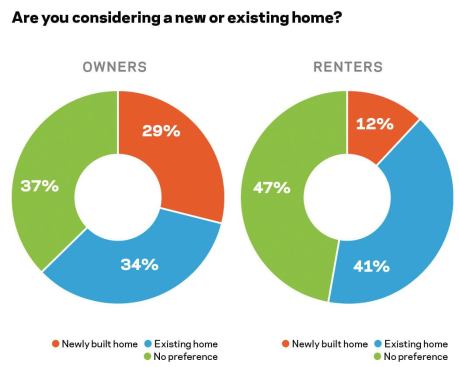

Builders really have their work cut out for them today, considering that more people prefer existing homes over new homes, and that those existing homes are perceived to be much less expensive. Even so, 29 percent of current homeowners would prefer to buy a new home, if they bought another. What do people like best about new homes? “Everything is new” was the top response, cited by 82 percent of current homeowners.

New homes have some practical advantages as well. Our survey shows that the next hottest buttons are low-maintenance and energy-efficiency. People are drawn by the opportunity to save precious time spent on home repairs, and they understand that a more efficient home will have a better chance to retain its value due to lower operating costs. It’s significant that these attributes finished higher than traditional drivers of new-home purchases—fresh floor plans and the ability to customize the home, though those finish high on the list, too.

Builders probably need to cover all these bases to get the sale in today’s environment. They not only need to offer the most energy-efficient home possible, but they also need to be flexible when it comes to customizing their plans. It almost goes without saying that floor plans need to be as compact and livable as possible. No builder can afford to create the impression of wasted space.

The survey was big enough that the results could be crunched by states, even by individual markets in some cases. In states hit hardest by the housing recession, California, Nevada, and Florida, for instance, most people still view homeownership positively. They think that owning a home is still important to their family and the economy.

After the birth of their first child, Cynthia and her husband moved from a condominium high-rise in downtown San Diego, where they barely knew their neighbors, to a home in the suburbs. Explained the 30-year-old, college-educated Native American: “For me, owning a home is a mark of stability in my life where I am set, grounded, and able to grow roots and let my kids be grounded and grow roots.”

Remarkably, most people still think homes are a good investment choice, even though home prices have fallen 35 percent nationally in the last several years. When asked about their home as an investment, most focus group participants didn’t see any better investment alternatives. Some people, such as Colleen, a single 36-year-old African American professional who owns her home and two investment properties in the Washington, D.C., market, saw a big opportunity.

“Give me the right deal and I’m in,” she said. “If the housing market goes down and even if you’re upside down on your mortgage, you still own something—you have a roof over your head or you can rent it out. It is something very tangible that doesn’t disappear. If your 401(k) goes to zero, you start all over again and you have nothing. Zero can’t grow.”

Things may be tough right now, says Colton, “but if builders can just hold on, they can look to a far better future. The study shows that for most Americans homeownership remains an important objective.”

The survey paints a sometimes bleak picture of the typical American’s ability to afford a home right now. Not only are people still feeling insecure about their job prospects, but many think mortgage lenders overreacted to the housing crisis by making it too difficult to qualify for a mortgage. Only about one-quarter of our respondents, for instance, said they could afford a 20 percent down payment.

“I think that the whole system was broken for years,” said a Des Moines, Iowa, homeowner, “and they were just giving away money because they were going to sell the mortgage … . There was no accountability. Now the pendulum has swung the other way, and it is really hard for kids to go out and buy a home.”

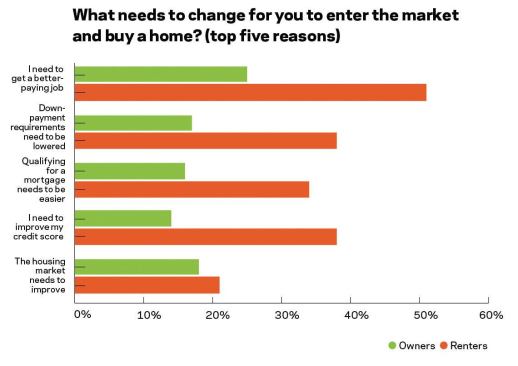

Renters in particular face some big hurdles to homeownership. When asked what needs to change to get them to move, 51 percent of renters said they needed to get a better-paying job. Twenty-three percent of owners said the same thing. The survey and focus groups turned up a reluctance to take a chance on a bigger, better home. “I would never sell what I have and move up to a bigger, more expensive house,” said one focus group participant. “I am safer where I am.”

One of the more puzzling questions in the housing market today is getting a good grip on how many families are doubling up to cut expenses and ride out the recession. “Judging from the results of this survey,” says Gopal Ahluwalia, a principal of the Colton Group who conducted the research, “the number appears to be high.”

A full 30 percent of our respondents were living with multiple generations at home. Adult-age, college-educated children without paying jobs are coming home to live with their parents. Grandparents are living with their grown children. And multiple families are living together because someone lost a job or their home.

The response to another question indicates that much of this doubling up may be short-lived. We asked about future plans to live with adult children or parents. Only 12 percent of owners, and 9 percent of renters, reported that their children would live with them. And only 13 percent of homeowners and 9 percent of renters reported that one or both of their parents would live with them.

Another big unanswered question in the housing market is how losses of equity and employment will affect retirement plans. About one-third of the population (31 percent) said that the economic situation had changed their plans to retire. Even so, people expect on average to retire at 66.

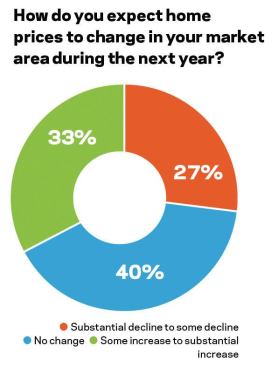

More than half of homeowners, 53 percent, have experienced some or substantial decline in home prices in their area during the last year.

Some older Americans no doubt want to recoup some lost equity before they move, since they don’t have to move right away. One in five of all owners (21 percent) stressed the need to recoup some of the lost value in their current home before reentering the market.

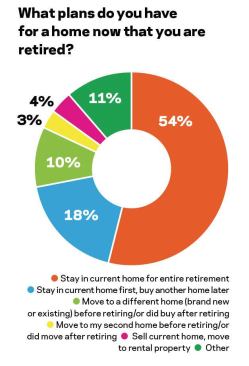

Retirement housing plans vary. Slightly more than half of respondents (54 percent) expect to stay in their current home for their entire retirement. Another 18 percent want to stay in their current home first then move later, and 13 percent plan to move to another home, or their second home, upon retirement, or had already done so.

When it comes to attitudes toward renting, the research results were tough to interpret. In focus groups, many renters professed to enjoy the freedom and flexibility of renting. One participant told us that he thinks there’s a generation gap when it comes to attitudes toward homeownership. “For younger people. it’s not a symbol [of prosperity] anymore. It’s a loser.”

That’s not what our quantitative research showed. Only 22 percent of renters think that renting makes better financial sense than owning. Most renters still aspire toward homeownership. More than half agreed that this would be a good time to buy. Young renters were significantly more positive about home buying conditions, with 65 percent of renters under 35 saying it is a good to very good time to buy.

The problem, as builders who cater to this group of potential buyers has found, is that many renters don’t have the money for a down payment. Less than 20 percent said they could make a 20 percent down payment. Most also said they don’t have the credit scores or job security to buy a home.

For that reason, most renters (62 percent) are resigned to the idea that their next home will be another rental. Even so, most people who rent don’t like where they live. Only 23 percent of renters are happy with their current residence.

Learn more about markets featured in this article: Des Moines, IA.