The fundamental driver of housing demand is the creation of new households. Counting the households that rent and those that own their home determines which sectors of the housing market are contracting or expanding. In the wake of the Great Recession, the average number of independent households grew by 539,000 annually, according to my analysis of Census Bureau data. This rate represented a decline from the 1.2 million average gain that existed from 2001 to 2007.

From 2008 to 2010, there was a shift in the source of these gains. The growth of rental households averaged more than 600,000 a year. Given that this figure is larger than the total expansion of households in this time frame, it’s not a surprise that the average change for homeowning households was a decline of over 100,000 per year—a result of foreclosure and a reduction of new home buyers, particularly among Generations X and Y.

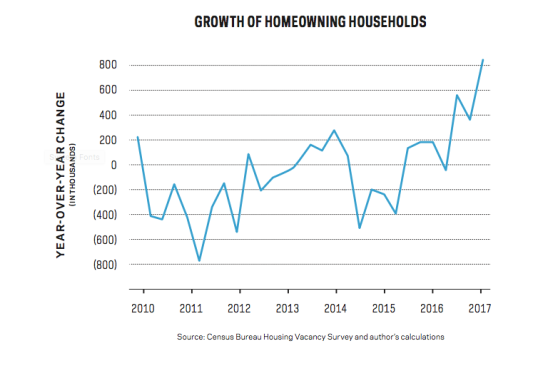

From 2011 to 2016, the negative growth of homeowning households ended, with the average annual change at roughly zero for those years.

During the five-year span, gains for rental households averaged almost 1 million per year. As such, the homeownership rate fell from 66.4% to 63.7%. Even in quarters when the count of homeowners was rising, the gains for renting households were larger, thus pushing the homeownership rate down.

The recent decline of the homeownership rate, which peaked at 69.2% in 2004, has led to some forecasts of further declines for the next 10 to 20 years. I think those forecasts are wrong because they confuse recent lack of means (wage growth and available inventory) with permanent changes in housing demand. Consumer preference surveys, including NAHB survey data, show solid support among younger Americans for single-family housing in the suburbs that they can own. For these reasons, I forecast that we are currently in a period in which the homeownership rate will stabilize.

Recent Census data provide preliminary confirmation of this and reveal what could be an important turning point. Over the past four quarters ending with the first quarter of 2017, the average annual growth in the count of homeowning households was more than 400,000. During the first quarter of 2017, the year-over-year growth rate of homeowners was 854,000, while the growth of renters was 365,000. The fact that both measures were positive is good for single-family and multifamily demand. Furthermore, the first quarter marked the first time since the Great Recession that the annual growth rate in homeowners was larger than the growth rate for renters.

Job growth, accelerating wage gains, and unmet single-family housing demand should see these trends continue. The question is whether the market can provide the right mix of supply as demand for single-family housing improves.