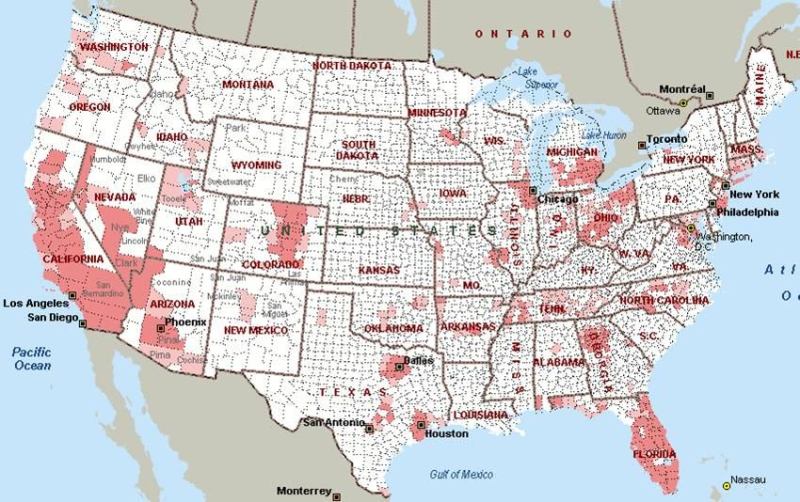

One in every 497 homes in the U.S. received a foreclosure notice in January, according to the latest data from RealtyTrac. In an industry that’s been battered by foreclosures since the housing bubble burst, the number may not seem like news, but these foreclosures are different.

Foreclosures today aren’t heavily dominated by investors that walked away from properties when values started to plunge. And they’re not the unfortunate folks who signed up for an adjustable rate mortgage they could no longer afford the first time their payments reset. Today’s foreclosure rates are ambulance chasers tailing the sirens of unemployment.

“You can almost follow county by county unemployment rates and foreclosures,” said Rick Sharga, senior vice president at RealtyTrac. “What’s driving this activity is the economic downturn and unemployment.”

And it doesn’t always take a dramatic drop in employment numbers to push a city into the red zone. “It’s really the direction of the unemployment rate that matters,” said Patrick Newport, U.S. economist with IHS Global Insight. “In some markets, it really doesn’t take much to topple them,” said Sharga.

This trend has wreaked havoc on real estate values in areas once thought to be stable, such as Seattle, where last year home prices plunged by more than twice the drop seen in Las Vegas during 2010, according to Zillow. While foreclosures are higher in Las Vegas, it—like many other red hot spots of the housing bubble—experienced the crash earlier on while the new trend in foreclosures is now spreading a new season of pain to places where the run up was less pronounced.

California, which had an unemployment rate of 12.5% at the end of 2010 according to data from the Bureau of Labor Statistics (significantly above December’s national average of 9.6%), produced seven of the 10 cities with the highest foreclosure rates in the country last month. The state accounted for 25% of all foreclosures in the nation in January.

To turn things around, Sharga says the markets would need both job creation and a return of consumer confidence. In the mean time, RealtyTrac is predicting that more than three million homes will receive notices this year and between 1.2 and 1.3 million of those will be repossessed.

The company is also keeping its eye on delinquency rates. “There are between $200 and $300 billion in adjustable rate mortgages readjusting this year … [to] much higher payments to marginally qualified home buyers who have lost 30%, 40%, or 50% of their home values,” Sharga says. “It could be a real mess.”

Claire Easley is senior editor, online, at Builder.

Learn more about markets featured in this article: Las Vegas, NV, Seattle, WA, Greenville, SC.