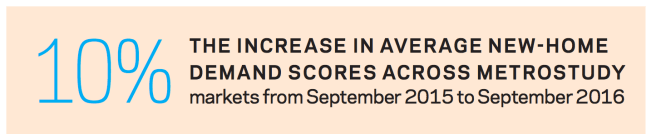

Our monthly demand index tracks builder demand for lots and buyer interest in new homes in 36 markets. The housing recovery has come a long way since September 2015; in September 2016, the average new-home demand score across all markets was 7.17 on our 10-point scale, 10.26% higher than a year prior.

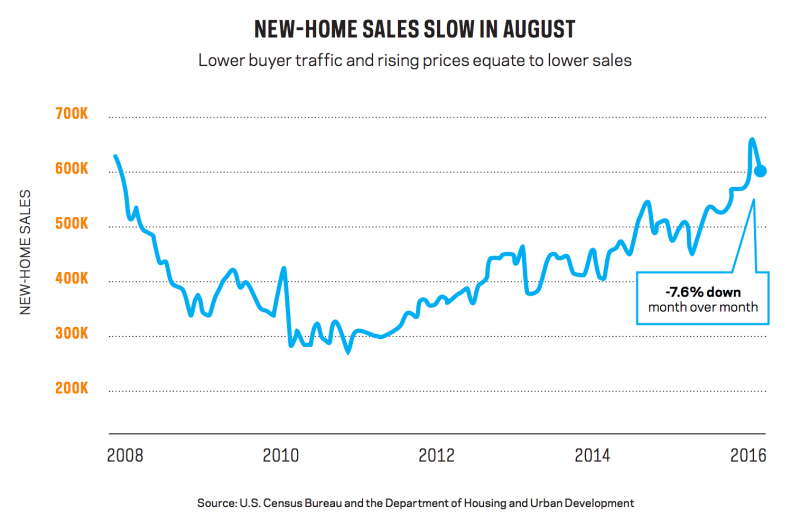

We’ve focused heavily on lot demand the past few months, as supply is tighter than ever and development costs have reached all-time highs. Price growth resulting from low resale inventory, and the need to turn a profit in the new home market, did not impact buyer traffic significantly in 2016 until September. After nine consecutive months of gains, average new home demand dipped -1.9%. Despite promising year-over-year gains, the dip echoes other economic indicators that slipped in August: residential construction spending decreased, and new home sales posted a -7.6% drop.

Metrostudy regional directors see no need to panic, however. Average new-home demand declined, but it’s more of a plateau when looking at individual market scores. Zero markets saw gains in September; five markets decreased while the others were flat.

Directors in Boise, Idaho, Charlotte, N.C., Philadelphia, and Salt Lake City attributed the 1-point dip to either seasonal slowdown or influence from the election. In Dallas-Fort Worth, the decrease could be cause for bigger concern. While seasonal shift could be at play, builders in the market reported less than stellar sales during June and July. According to regional director Paige Shipp, this could indicate the market has hit a price ceiling after years of double-digit appreciation.

“Interestingly, sales have been generally slower across all price points, which is counterintuitive to [that] argument,” Shipp says.

As a major market in our index, the story in Dallas-Fort Worth could be a sign of things to come in other major markets. However, it might be uncertainty about the economy, rather than price, that will be the biggest impediment for housing in the future