With existing-home sales rising for five of the last six months, foreclosure sales seemingly on the decline, new-home sales prices firming, and the economy growing again, it looks like the home building industry may be safely out of the woods. But, as any self-respecting two-handed economist will tell you, there are several lurking economic demons that could pounce on an industry that thinks it has reached a clearing.

It’s hard not to listen to the warnings, because the history of this housing recession is one of dashed hopes. Several times, expectations have risen only to be mercilessly crushed. First it was the subprime fiasco, then the global financial recession of September 2008, and more recently a foreclosure crisis. What’s next?

Try a collapse in the commercial real estate market. If that proves calamitous, the FDIC may need a lot more paper to print its list of bankrupt banks. Other lenders, worried about their exposure, may be unwilling to lend even when builders identify can’t-miss projects. Then there’s the possibility of a sizable increase in foreclosures due to the pending resetting of mortgages taken out by second-home buyers and well-to-do investors, who may not be as well-heeled anymore. And questions persist about the impact of prolonged, high unemployment on home buying decisions.

For all of the above, economists are pretty much of one mind that home building will not snap back as quickly as it did after previous housing recessions, despite November’s 8.9 percent increase in starts. The recovery is likely to be slow, which will make this one unusual. In a study of the five housing recoveries since 1960, housing starts rose 50 percent from the trough during the following year, according Fitch Ratings. Fitch is only looking for a 16 percent starts increase next year, one of the most bearish predictions around.

The NAHB estimates that housing starts will rise 24 percent in 2010 to 695,000. At that paltry level, production would remain 22 percent below 2008’s 900,000 homes. Why such a slow pace? Bernard Markstein, who leads the forecasting group at the NAHB, easily produces a list topped by “excessively high” mortgage approval requirements, non-comparable appraisals, and naggingly high unemployment. The good news, he says, is that some of these negatives should lessen during 2010, setting up 2011 for a big recovery. The NAHB predicts a 50 percent surge in starts that year.

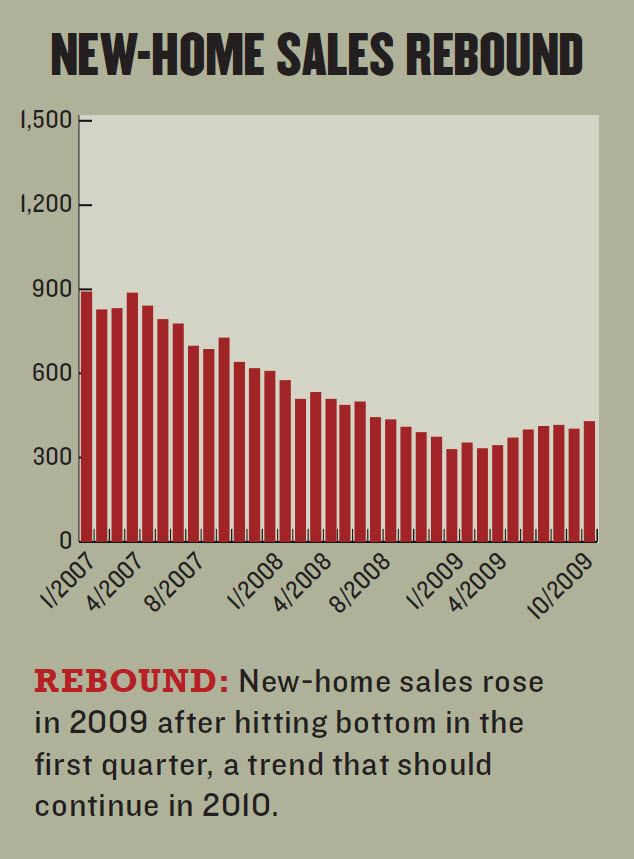

The industry’s prospects would have been much worse had the federal government not extended the $8,000 tax credit for first-time buyers through April. Moreover, the addition of a new $6,500 tax credit for people who have previously owned a home may wake the moribund move-up market.

Homes Are Where the Jobs Go at Night

Even so, the job situation has economists wondering whether the housing market is standing on wobbly legs. “We expect a very modest recovery in home building because underlying demand remains weak,” says Mark Vitner, managing director and senior economist at Wells Fargo Securities in Charlotte, N.C. Vitner projects only an 18 percent increase in home starts this year. He believes last year’s tax credit stimulus provided an unsustainable lift, robbing sales from 2010. “A sustainable recovery will not take hold until employment conditions improve significantly,” he says.

Though he regularly produces the most pessimistic housing forecast, Mark Zandi, chief economist for Moody’s Economy.com, still managed to shake up the NAHB’s fall forecast conference by saying that the market will have another leg down. Zandi’s pessimism stems from persistent unemployment coupled with foreclosure filings, which he believes will rise in the spring and summer, depressing home prices. “Prices have stabilized, but I don’t think price declines are over,” he said.

A more bullish forecast comes from IHS Global Insight, which projects 850,000 housing starts, a whopping 49 percent increase. Inventory is so low, IHS believes, that builders will need to go vertical to meet rising demand. “In 2010, job growth, low inventory levels of new homes (currently at their lowest point since 1983), and household formation will result in sustained increases in housing starts,” says Patrick Newport, the firm’s U.S. economist.

The consensus forecast, however, is for something in between. The National Association for Business Economics (NABE), which produces an average forecast based on submittals from 48 professional forecasters, is calling for 790,000 starts this year, a 36 percent increase. “2010 will be the first year since 2005 that the housing sector will contribute to overall growth,” the group reported in November.

Painting an Employment Picture

Even if starts rise by a third, it will take the economy a long time to fully recover from staggering unemployment. Though monthly job loss totals slowed dramatically in late 2009, and unemployment actually declined to 10 percent in November, total employment has fallen to levels last seen in 2004. All the job gains of the last five years essentially were wiped out.

“The employment situation still looks incredibly dire,” says Vitner. “We are on a pace to lose 9 million jobs in this recession, and it will likely take until the middle of the next decade to replace those jobs.” NABE’s consensus forecast calls for 9.6 percent unemployment this year.

Vitner points out that even as jobs are replaced, many recently employed won’t be in a position to buy homes. Roughly one-third of the unemployed, he notes, have been out of work for six months or longer. They have likely exhausted their savings. “If they get a job tomorrow, they’re not going to be able to go out and make big purchases. They’ve got a heck of a hole to fill.”

Learn more about markets featured in this article: Charlotte, NC.