Headwinds–macroeconomic crosscurrents, global trade dislocation, and chronic supply constraints–are roiling the business environment and creating choppy and iffy market conditions for single-family players. In the weeks and months ahead, the smarter ones will shift their focus to outlier opportunities. For outliers, excellence–not average performance–is a difference-maker. It’s a marker of resilience when, not if, adverse forces gather momentum. Many outliers, as it so happens, leverage data as a path to detect opportunity that others can’t spot.

A defining dynamic of housing economics is this: people’s household wages barely budge, while hard and soft costs to builders soar. Common denominators for success or failure for builder firms as this dynamic plays out and times get tougher boil down to both the simplest and the hardest two questions to answer and act on affirmatively.

- Can we build the right house?

- Can we build the house right?

Both of these questions presuppose a capacity among builders, developers, investors, and their partners to use precious resources to put vertical value on dirt that’s predictably and profitably greater than the lump-sum costs of doing it. And do it again and again. The “right house” means a home product that fits the location, a community that fits lifestyles and customer segments, and an asking price range that fits the financial tolerances of would-be buyers in that geography.

“Building the house right” means that balance of durability, function, aesthetics, and attainability that confer value to the one(s) paying to live there. Meeting inhabitants’ needs for everything from the experience of sanctuary, to the feeling of safety and security, to the assurance that one’s total-cost-of-ownership nets out positive over time, to the sensation of confidence that all is working as it is meant to add up to well-being, a measure of a home’s value in real-time and across time.

Late-housing-recovery-stage tides tend to be ever-more stingy about “lifting all boats.” The outlying opportunities may lie in atypical resilience or strength in a submarket, or, for example the imminent arrival of the second headquarters of one of the biggest companies in the world in a market, or a consumer migration and housing preference trend that has pronounced itself as noteworthy over the past decade or so.

So, if the market becomes “choppy,” how do you navigate timing of capital outflows and upfront investments to smooth absorption pace and operate with less exposure to volatility risk?

If the market becomes “spotty,” how do you locate your investments and communities where steadier demand pull can normalize volume and pace and continue to pull through overhead costs per the model?

Finally, if the market turns “iffy,” how nimble can you be at dialing down risks and exposure altogether until the first signs of conviction return to the markets?

Data–and the willingness to listen to it and act on it–is certainly part of the answer to all three questions.

Check out National Association of Home Builders assistant VP for forecasting and analysis Danushka Nanayakkara-Skillington’s piece on across-the-board declines in single-family permits in 2019 versus last year. Nanayakkara-Skillington writes about the negative growth this way:

Year-to-date ending in May, single-family permits reported declines in all four regions. The Midwest, West, South, and the Northeast declined by 10.6%, 11.0%, 2.8%, and 1.9% respectively, compared to the same time period in 2018. The Southern region had the highest growth in multifamily (12.7%) while the West recorded a decline in multifamily permits growth (-4.6%) during the last 12 months.

Between May 2018 YTD and May 2019 YTD, nine states and the District of Columbia saw growth in single-family permits issued while 40 states registered a decline. Minnesota reported no change. The District of Columbia recorded the highest growth rate during this time at 110.2% from 49 to 103 while single-family permits in South Dakota declined by 25.0%, from 1153 in 2018 to 865 in 2019. The 10 states issuing the highest number of single-family permits combined accounted for 61.5% of the total single-family permits issued.

Now, why is this interesting?

It is so at least in part because the map gives visual and geographical evidence to show that, outside of pockets of strength expressed in commentary by public builder executives during recent earnings announcements with investors, overall new single-family construction activity is slowing down. Almost everywhere. The Census’ mid-July starts and permits release shows permits lagging June 2018 levels by 6.6%.

Nanayakkara-Skillington’s heat map for declining permits might be considered a study in contrasts with the way home builder confidence is trending, as evidenced in yesterday’s release of the NAHB/Wells Fargo Housing Market Index, which rose one point to 64.

Builders may be confident, and may be factoring in some of that confidence based on wide expectations of the Federal Reserve to further lower interest rates to stimulate more activity. But they’re going to have to be more than confident.

They’re going to have to be smart and to stand out.

Enter data, a way to find a path through “choppy,” “iffy,” and “spotty” market challenges that lay ahead.

For instance.

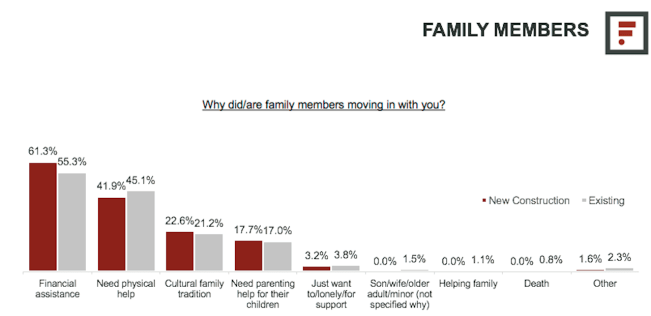

Unpack Pew Research analysis of Census Bureau household demographic data that shows that 64 million Americans now live in multigenerational households–defined by more than one generation of family-related adults under one roof.

Ask them why they choose to live in multigenerational households, as we did, and you’ll find that a majority of multigen household adults are living that way “for financial reasons.” Those financial reasons may vary widely. It may be about the wherewithal (i.e. limited) of the younger adults; it may be about a sandwich generation adult losing his or her job; it may be about an elderly family member needing ongoing caregiving, etc.

In an era defined by the widening gap between income growth and housing costs, the litany of financial reasons can be extensive.

We’d bet there’s a similar motivation at work in a datapoint BUILDER sibling Meyers Research’s director of economic research Ali Wolf and her team have developed, the Baby Chaser Index, featured here on Marketwatch, in a piece by correspondent Alessandra Malito. This metric, as its name suggests, plots a notably strong correlation between Millennial and Baby Boom migration patterns. The inference–one that has very strong land strategy, community development and planning, pricing, and product configuration implications for developers and builders–is that, where young early-forming families are heading, there, the older, retiring generation of parents will gravitate.

Here’s commentary from our Meyers market insight masters, Ali Wolf and senior managing principal Tim Sullivan.

Baby Boomers are often looked at as moneybags, but affordability is a top factor for homebuyers regardless of age. For those leaving their current city, retirees are often looking to sell their home, relocate, and pocket some money. That success depends on where they are coming from. In our top Baby Chaser market, Charlotte, for example, Rust Belt state relocators more frequently enter with less equity than those from New York. That’s why it is important to measure not only where people are moving to but also where they are coming from.

“The secret sauce for this homebuyer connects back to key drivers for the active adult market: 1) the ability to move down in size but not quality, and 2) pay for the new home with proceeds from the sale of a previous home with some cash left over. What differentiates the Boomer buyer from their parents’ retirement process is that the Boomer is moving to, not away, from the kids,” explains our Senior Managing Principal, Tim Sullivan.

And the take-away here is that you can use data to map a macro trend–the “for-financial-reasons” motivator for older and younger generational synchronized mobility–into an outlier read on where the market will move. Even as things get tougher on average.

Remember, too, some sage counsel from the late Steve Jobs when you think about the role of data and its ability to help you and your team become excellence outliers. He said:

“What’s important is that you have faith in people, that they’re basically good and smart, and if you give them tools, they’ll do wonderful things with them. It’s not the tools that you have faith in–tools are just tools.”