With housing costs rising and no signs of a deceleration, first-time buyers are turning to family for help when embarking on homeownership. In spite of this, the percentage of first-time buyers remains at historic lows.

This is according to a new report from the National Association of Realtors, the 2019 Profile of Home Buyers and Sellers, a yearly report which covers demographics, preferences and experiences of buyers and sellers across America. The full report will be released Friday, Nov. 8, at the Realtors Conference & Expo in San Francisco.

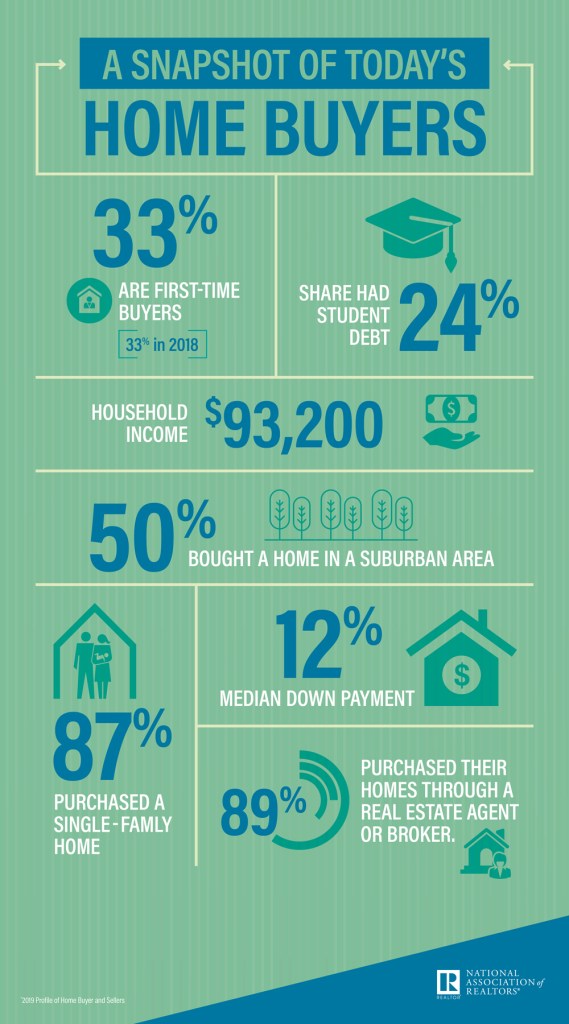

Initial results from this year’s report revealed that a third of first-time home buyers used down payment help from family and friends. Also, it showed that the share of first-time home buyers remained at 33% in 2019. This figure continues to be below the historical norm of 40% of recent primary residence home buyers in the market.

“Pre-recession, the number of first-time buyers was higher, in part, because buyers had more options,” said NAR President John Smaby, a second-generation Realtor from Edina, Minnesota, and broker at Edina Realty. “However, over the past few years, we have unfortunately experienced a scarcity in housing inventory, especially at the middle- and lower-end of the market.”

Citing the NAR survey, NAR chief economist Lawrence Yun noted that buyers report the most difficult step in the home buying process is just finding the right home to purchase, and what buyers want most from their real estate professional is to help them find the right home to purchase. “Low inventory conditions hurt would-be first-time buyers most,” said Yun. “Their homeownership dream and the opportunity to build wealth gets delayed until more inventory choices reach the market.”

Although tightened inventory has taken a toll on home seekers and caused steeper housing prices, home sellers in many areas of the country have been able to take advantage of these conditions. Sellers saw a very favorable market this year. In fact, home sellers received a median of 99% of their asking price this year and sold their homes typically within three weeks.

The increase in home prices lowered the amount of home sellers who reported delaying selling because their home was worth less than their mortgage. This particular share of sellers declined from 9% in the 2018 report to 7% in 2019. However, 20% of sellers who bought their home 11 to 15 years ago continue to report stalling their home sale.

A Change in Home Buyers’ Behaviors

The NAR report found that the share of new homes purchased dropped to an all-time low of 13%. This reality offers yet another indication of a significant deficiency in inventory. Also, 23% of first-time buyers moved from a family or friend’s residence directly into the home they purchased. This figure represents nearly twice the historic rate of 12%. It serves as another example of home buyers adjusting to the current housing market and shows they’re finding ways to save for a down payment while saving on market value rent.

Additionally, the age of repeat buyers – which has steadily increased over the course of several decades—continues to show a striking trend. The average repeat buyer age was in the mid-30s in the 1980s, and has climbed to the mid-50s today. Yun said there is no area that has seen a more rapid and consistent increase than the median age of repeat buyers—which hit a record-high of 55 years old in both 2018 and 2019.

Moreover, the median age for first-time buyers increased to 33 years old in 2019, the highest share recorded in the series’ history. Still, the share of senior-related housing purchases was 12% in 2019, a slight decline from one year ago.

As prices crept higher, Yun said the demographics of home buyers shifted as well. “Buyers and sellers, individuals and families—they all had to adjust to changing market conditions.”

Underscoring Yun’s point of a shift in demographics, the survey revealed that 35% of all buyers had children under the age of 18 living at home. This is an increase from 34% last year, but a drop from a high of 58% in 1985. 12% of home buyers purchased a multi-generational home, which consists of a home with adult siblings, adult children over the age of 18 and parents or grandparents—or both—within the same household.

Respondents gave varying reasons for buying multigenerational homes, including 44% to accommodate aging parents and 34% to accommodate adult children in the home. Another 29% referenced cost savings as their reasoning.

The share of married couples who purchased their first home continued to decline from a historical high of 75%. Although the percentage of married repeat buyers remained constant at 67%, the share of first-time buyers who were unmarried couples rose to a historical high of 17%. Those purchasing first homes as roommates jumped to 4% from 2%—another example of buyers seeking ways to enter ownership with affordability constraints.

Survey results show that 14% of recent home buyers own more than one home, down from 17% in 2018. Home buyers who have higher incomes and own more than one property are more commonly making home purchases, the report said. Owning more than one property was the most common for home buyers 65 years old and older, at 19%.

Overall, the internet has become the main source for buyers in terms of finding a home that they ultimately purchase. Today, 52% of recent buyers found their home while searching online, an increase from last year’s 50% share. In 2001, only 8% of buyers found their home this way. Finding a home through a Realtor or an agent has shifted from being the most common source for finding a property to the second most common. While more traditional sources—yard signs, relatives, neighbors, friends, and home builders—remain at last year’s levels, they all have declined as a primary source throughout recent years as the internet has become the go-to information source.

Embracing Industry Changes

While the housing market has certainly endured its share of changes and transitions, especially over the last year, the NAR report shows that many of these changes have had positive impacts. This is especially true in regard to the home down-payment requirement. In 2019, the median down payment was 12% for all buyers, 6% for first-time buyers, and 16% for repeat buyers. Lower down payments among home buyers are another result of rising home prices as buyers find it difficult to save for a down payment. Seventeen percent of all buyers and 25% of first-time buyers used an FHA loan to purchase, likely taking advantage of low down payment programs.

NAR’s survey asked home buyers about their personal experience with securing a mortgage. In 2019, 31% said obtaining a mortgage “was more difficult than expected.” Although a considerably higher number of people had this same answer in 2009 and in 2010, fewer respondents have this response every year since, including this year, according to the report.

“Today, repeat buyer behavior is more similar to first-time buyer behavior as tenure in home has increased,” said Jessica Lautz, vice president of demographics and behavioral insights at NAR. “All buyers are doing their homework—going to open houses, following housing news—and are more reliant than ever on the expert advice of real estate agents and brokers.”

Characteristics of Sellers

The typical home seller this year was 57 years old, with a median household income of $102,900. Home sellers said they ultimately sold their homes for a median of $60,000 more than the price they paid for it.

For all sellers, the most frequently cited reason for selling, according to 16% of those surveyed, was a desire to move closer to family and friends, which is the first time this has been the top-cited reason in the series’ history. The next most common reason was that the home was too small, and the third was job relocation at 11%. Sellers typically lived in their home for 10 years before selling it, an increase from last year’s share, and elevated from the historical tenure of six years.

66% of sellers reported being “very satisfied” with the overall selling process. Only 8% of recently sold homes were for-sale-by-owner sales, or FSBO. This total is near the lowest share recorded since the NAR began collecting records in 1981. The median age for FSBO sellers is 60 years, while 65% of FSBO sales were by married couples that have a median household income of $94,000. FSBOs typically sell for less than other residences, selling at a median price of $200,000 last year, while homes sold with the assistance of an agent reached a median sales price of $280,000.

48% of all sellers said they bought a home that was newer than their previous home, while 28% purchased a home the same age and 24% said they purchased a home that was older. 44% of sellers said they “traded-up” and purchased a home that was more expensive than the one they just sold. Thirty percent purchased a less expensive home and 26% purchased a home that was similar in cost. Sellers who are 64 years of age and younger generally bought a more expensive home than the one they just sold. Those aged 18 to 34 purchased the most expensive trade-ups in 2019, recording an increase of $110,000. Conversely, sellers aged 65 and over typically bought a less expensive home.

About NAR’s Survey

NAR mailed a 125-question survey in July 2019 using a random sample weighted to be representative of sales on a geographic basis to 159,750 recent home buyers. Respondents had the option to fill out the survey via hard copy or online; the online survey was available in English and Spanish. A total of 5,870 responses were received from primary residence buyers. After accounting for undeliverable questionnaires, the survey had an adjusted response rate of 3.7%. The sample at the 95% confidence level has a confidence interval of plus-or-minus 1.28%.

Recent home buyers had to have purchased a home between July 2018 and June 2019. All information is characteristic of the 12-month period ending in June 2019 with the exception of income data, which are for 2018.