Nine years into tracking millennials, it is clear that a tidy narrative should not be forced. Millennials, broadly defined as those born between 1980 and 2000, are increasingly split between two distinct housing realities. Some bought young, before 2022, and are now sitting on substantial equity gains, but remain effectively locked in at low mortgage rates. Others missed that window and are now looking at a housing market that feels permanently out of reach. In many ways, this divide has become the defining millennial housing story of 2026.

But the generation is not static. Family formation, lifestyle changes, employment shifts, and affordability pressures are all also influencing where and how millennials want to live. This year’s survey reinforces a line that has held across nearly a decade of research: millennials still want to own homes, if they don’t already, but are becoming more flexible, largely out of necessity, when it comes to how and when they pursue that goal.

Zonda’s ninth annual millennial survey, conducted from December 2025 through January 2026, drew roughly 1,000 responses across 43 states, with California, Texas, Florida, New York, Ohio, and Pennsylvania the most represented. Among the respondents, approximately 70% were married, 70% had children, 60% already owned their home, and 30% were considering relocating over the next year, whether for employment, lifestyle, cost, or other reasons.

Mixed Employment Setups

For the past several years, remote and hybrid work has been central to understanding millennial housing behavior. The shift away from traditional offices has fundamentally changed housing market dynamics, fueling suburban migration, expanding households’ search radii, and, in many cases, loosening the link between where households live and where they work.

Source: Zonda

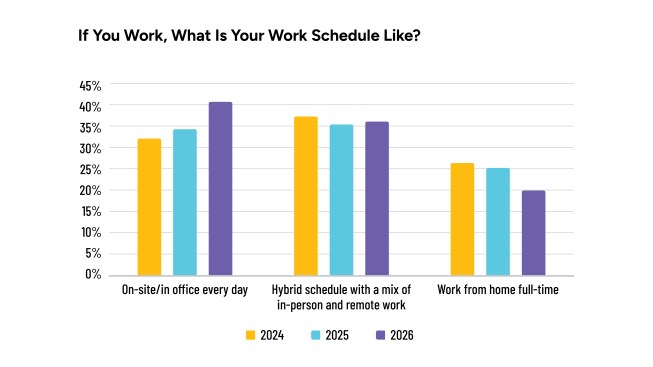

That influence has carried into 2026, with approximately 56% of employed respondents working either hybrid or fully remote schedules. While that share has declined from both pandemic highs and more recent years (61% in 2025 and 64% in 2024), it remains far above historical norms and continues to influence housing choice. Perhaps the clearest indicator of how thoroughly work from home (WFH) has decoupled geography from employment: 17% of remote and hybrid workers reported that their employer is located in a different city or state.

Survey responses related to commuting patterns further reinforce this shift. Some millennials live within short distances of their workplace, often prioritizing walkability, convenience, and proximity to amenities. Others tolerate commutes of 50 minutes or more, particularly when remote schedules reduce the number of required office days.

There’s also a clear divide when it comes to housing type: renters tend to live closer to their office than homeowners, reflecting both preference and constraint. For some, proximity is a lifestyle choice. For others, it is a function of affordability, with homeownership often pushing households from core office locations.

The broader implication is that remote and hybrid work continue to expand geographic choice, with location decisions no longer always dictated by office proximity. But this is another line that divides the generation. Millennials tied to traditional office schedules, especially non-owners, still appear to prioritize work proximity. Those with remote or hybrid flexibility are weighing cost of living, lifestyle desirability, and long-term financial goals in ways that would have been far less common a decade ago.

Financial Progress With Ongoing Strain

An uncomfortable truth about millennials in 2026 is that, by most objective measures, they should be in a strong financial place. Income growth has been positive for much of the cohort over the past year, with most households reporting either stable or increasing earnings, despite a more challenging employment landscape. That said, financial progress is uneven across the generation and is often offset by rising housing costs and higher overall cost of living.

This dynamic tracks when looking at savings behavior: just over half of respondents reported that they were able to save more this year than last, while the remainder saw little to no improvement. Notably, the ability, or perhaps the willingness, to save more was markedly higher among respondents with children and among homeowners.

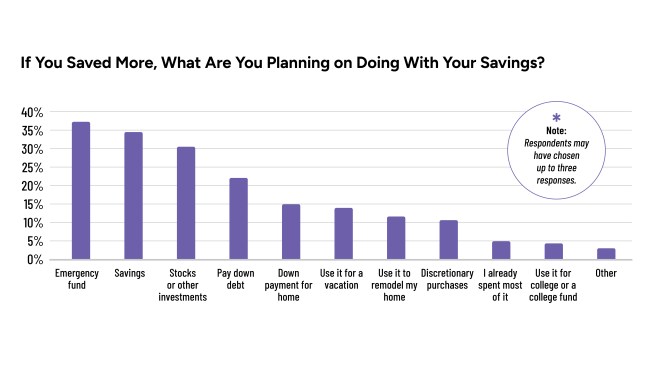

For those who did manage to increase savings, the top priority was building an emergency fund (37%), reinforcing a continued focus on financial stability. Beyond that, several other behaviors stood out among this group, each carrying direct or indirect implications for the housing market:

>Keep saving as much as possible (34% of respondents).

>Stock or other investments (30%).

>Pay down debt (22%).

>Use for down payment on a home (15%).

>Use it to remodel my home (12%).

Taken together, these behaviors and survey results suggest that many millennials are financially healthier on paper. Yet despite this progress, a meaningful share still feels financially exposed.

Source: Zonda

Homeownership Remains the Goal, but Tradeoffs Are Expected

Despite these pressures, the generation’s desire to own remains firmly intact. While ownership rates among surveyed millennials were already relatively high, renters consistently cite affordability pressures in preferred locations, challenges saving for a down payment, and a desire to remain flexible as they assess market conditions as their primary reasons for delaying a purchase.

Importantly, very few renters describe their housing situation as a long-term lifestyle choice. For many, renting is seen as a temporary or strategic decision, allowing them to preserve liquidity, invest elsewhere, or hold out for a more favorable entry point into the market. This distinction matters for housing demand, as it suggests significant pent-up ownership interest rather than a structural shift away from buying.

At the same time, many millennials demonstrate a high willingness to adjust their original expectations in order to buy. They’ve expressed that they’re open to exploring neighborhoods they hadn’t previously considered, relocating within their current state, or moving to an entirely different state in search of affordability. Others are willing to accept smaller homes, fewer amenities, or simply stretch their budgets further than planned.

That willingness to stretch shows up clearly in the numbers. Among renters, over three-quarters said that they’d be willing to pay more each month to own than they currently pay to rent. The largest share (17%) would go up to $500 more per month on a mortgage, with another 15% willing to pay up to $1,000 more.

This raises a natural next question: if millennials are willing to make tradeoffs, what are they prioritizing in return?

What Millennials Actually Want

As millennial households continue to evolve, their housing preferences reflect a blend of practical and lifestyle considerations. The core features they prioritize have not changed meaningfully in 2026, with large backyards, garages, usable outdoor areas for socializing, dedicated office space, and pools remaining among the most frequently cited preferences. Kid-friendly layouts, storage, and flexibility continue to matter as well.

What has changed, however, is how explicitly respondents are connecting their preferences to affordability when describing their ideal home. Many emphasize that they don’t need high-end finishes or extensive amenities; they want homes that feel somewhat aspirational, but that meet their needs without overextending their finances. Several went further, directly calling out the gap between what’s being built and what would actually serve them.

Related, while energy efficiency remains a priority for most millennials, willingness to pay for it is more limited. Many respondents say energy-efficient homes and appliances matter to them, yet only a subset is willing to absorb a significant price premium.

Differences between renters and homeowners also became evident when digging into living space. Most homeowner respondents live in homes between 1,500 and 2,500 square feet, with a growing share in larger homes as move-up activity continues to gain generational momentum. Most millennial renters, by contrast, remain concentrated in smaller units between 1,000 and 1,500 square feet (37%). That space gap reflects both affordability constraints and where each group is at in their housing journey.

In terms of a neighborhood wishlist, millennials see relatively little response variation across birth years and remain broadly aligned with other demographic cohorts. Access to restaurants and retail, safety and low crime, proximity to work, and walkability consistently rank among the top priorities. For households with children, access to parks and nature, along with quality schools, stands out. Finally, proximity to family also continues to matter, reflecting both emotional considerations and the practical role of support networks.

Taken together, millennial preferences continue to favor connected, well-located, mixed-use communities. Even though many millennials retain some flexibility in where and how they work, closer-in locations have outperformed in recent years, suggesting that proximity still carries weight and matters, just in more nuanced ways than before.

Strategic Builder Implications

Millennials are no longer emerging buyers. They are the backbone of housing demand, but increasingly split between those who have already secured a foothold in the market and those still trying to enter. While today’s environment is challenging, the 2026 survey highlights a generation that’s pragmatic, flexible, and still strongly motivated to own homes, even as the path to ownership becomes more complex.

The opportunity for the housing industry is not to convince millennials that homeownership matters, as that demand is already there. Instead, the focus should be on meeting them where they are by delivering homes and communities that reflect the realities they are navigating today. That means prioritizing price attainability, using space more efficiently, and designing homes that allow for flexibility as households navigate tradeoffs across price, location, and lifestyle. Builders that can adapt product to these constraints, without sacrificing functionality or perceived value, will be best positioned to convert interest into sales.

Ultimately, the millennial housing story is defined by a widening divide between those already in the market and those still trying to break in. How this gap is bridged is what will define the next phase of housing demand.

Sarah Bonnarens contributed to this article. The insights in this article were taken from more in-depth research reports published in Zonda’s National Outlook subscription.