There are many ways to build wealth, some more daunting than others. While stocks and bonds can be great investment vehicles, the most tangible investment for most people is homeownership.

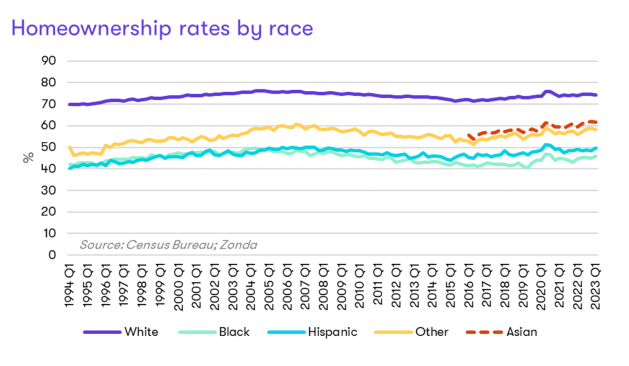

When looking at the United States, however, it is clear that access to and education around homeownership varies by race. For example, the homeownership rate for white families—ranging from 70% to 80% over the past 30 years—has historically been higher than the homeownership rate for other races.

The white homeownership rate stands at 74%. Conversely, the homeownership rate for the Asian population is 62%, 50% for Hispanics, and 46% for Black households. We show Hispanic as a racial group, although this is technically not a race, according to the U.S. Census Bureau.

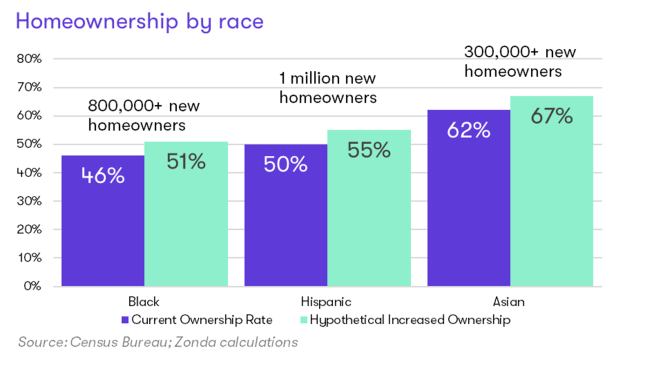

From a business perspective, increasing the homeownership rate for underserved communities would be a massive boost to the real estate industry. For instance, if the rates were increased by a relatively modest 5 percentage points for Black (from 46% to 51%), Asian (from 62% to 67%), and Hispanic (from 50% to 55%) families, this would create an increase in demand of over 2 million housing units.

With the Black homeownership rate the lowest among the cohorts with little improvement over the years, we think it is important to provide context regarding locational differences, historical factors, the human impact, and potential solutions to bridge the gap.

Locational Differences

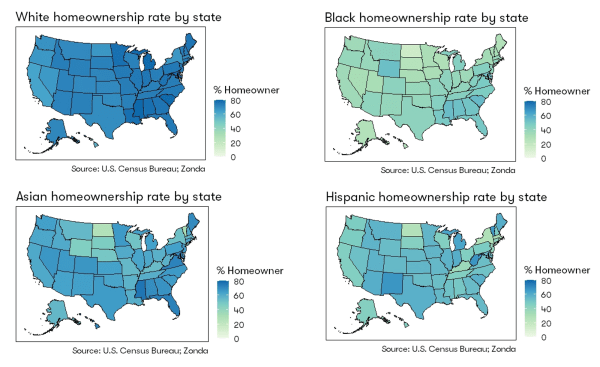

Below is a collection of graphs that show homeownership rates by racial group across the United States. All of the graphs are on the same scale for comparability.

- Regardless of racial makeup, the top three states for the highest homeownership rates are West Virginia (76%), Maine (75%), and Minnesota (73%). The lowest states for homeownership across the country are Nevada (58%), California (53%), and New York (52%).

- The white homeownership rate is the highest in Delaware, Mississippi, and South Carolina at 81%, 80%, and 79%, respectively. The highest homeownership rates for Black individuals are also in Delaware (54%), Mississippi (54%), and South Carolina (55%), but at a much lower level compared with the white rates.

- The lowest homeownership rates for Black individuals are in Alaska (27%), South Dakota (25%), and North Dakota (15%).

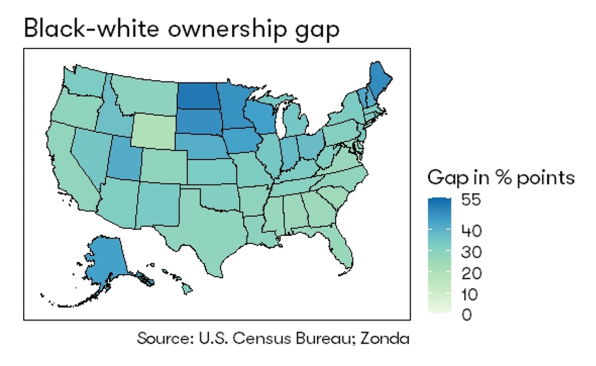

We can also look at the Black-white ownership gap by state (see graph below). The gap is substantial across the entire United States, with Wyoming having the smallest Black-white gap at about 20 percentage points. North Dakota has the largest gap at approximately 52 percentage points.

Among medium to large cities, the smallest gaps are in Oxnard, California (17 percentage points); Colorado Springs, Colorado (18 percentage points); and Charleston, South Carolina (18 percentage points). The largest gaps are in Worcester, Massachusetts, and Minneapolis, each at 45 percentage points, and Salt Lake City at 47 percentage points.

With the racial differences in homeownership apparent, it is important to examine the factors that have contributed to the disparity.

What Got Us Here?

Many historical factors have contributed to the racial disparities in the United States. Some damaging examples include:

Racial covenants. Early in the 20th century (circa 1910-1920), racial covenants restricting sales of homes to non-whites emerged. These covenants were a precursor to redlining.

Racial covenants were legal documents that stated that the owner of a given property would not sell or rent to people of certain races. These covenants were often used to create “white-only” communities; some went so far as to openly state “Aryans only.”

These racial covenants remained in place until 1968, when the Fair Housing Act explicitly banned racial discrimination in homeownership. However, the effects of these policies are still being felt as non-white families typically had a more difficult time buying homes and participating in the wealth building of homeownership.

Redlining and the Federal Housing Administration (FHA). The FHA was created to help boost homeownership during the Great Depression. Unfortunately, access to FHA loans turned out to be discriminatory in the early years given redlining practices. The term “redlining” comes from red areas on FHA maps that were classified as undesirable. The redlined areas were typically the sections of cities with large amounts of Black or non-white residents. There was a class element to this as well, with some poorer white areas also viewed as undesirable. Banks were discouraged from originating mortgages in these areas as the loans were perceived as less likely to be paid back (although this perception had no basis in fact). Redlining lending practices created areas that became chronically underserved in mortgage financing as well as economically underdeveloped. This not only negatively impacted non-white households directly at the time, but also created disparities in wealth and assets that are still present today.

GI Bill. Other programs, such as the Servicemen’s Readjustment Act of 1944 (commonly known as the GI Bill), that were intended to help veterans buy homes were also plagued with racial discrimination. The GI Bill did not have explicit racial restrictions built into it, but, since parts of the U.S. were still segregated when the bill was passed, many Black vets returned to limited educational opportunities or were denied loans from the predominately white-operated financial institutions.

Other discrimination. Although the examples we cite are primarily related to housing, the driving force behind the various elements of discrimination in the U.S. stemmed from the general social climate of past eras. Slavery massively impacted the ability of Black families to generate wealth. Even after slavery was abolished, the variety of anti-Black laws passed in the late 1870s onward, informally known as Jim Crow laws, also hurt the ability of Black families and individuals to accumulate wealth.

The Human Impact

We already mentioned that a modest boost in the homeownership rate among Black, Asian, and Hispanic families could drive demand for over 2 million housing units. Why do we care?

Beyond the basic indecency, we know that an inability to get on the homeownership ladder can have long-lasting effects. Housing offers many benefits to owners, including stability, fixed payments, the potential for home price appreciation, a savings path for retirement, and the longer-term benefit of generational transfer of wealth.

In fact, housing wealth is a key component of financial well-being for middle-class families, typically making up over one-third of their total wealth (“Importance of Wealth,” p. 4). The Federal Reserve, among many other organizations, has researched the racial wealth gap in the U.S., showing large disparities between racial groups in terms of wealth. Increasing access to homeownership is a significant driver of wealth building, especially for families of color (“Importance of Wealth,” p. 7).

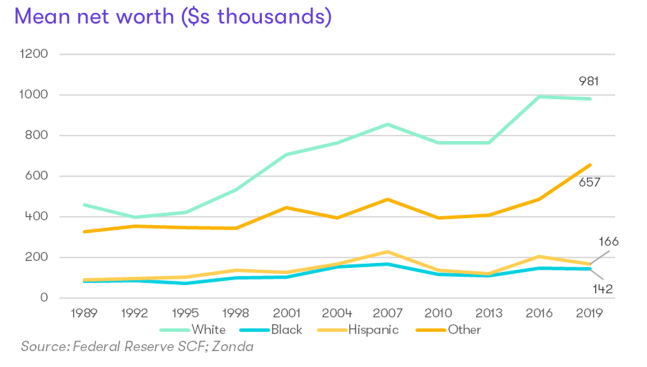

We can see the data from the Federal Reserve’s most recent Survey of Consumer Finances completed in 2019 (below), which shows clear differences by race:

- The mean net worth of white households was about $981,000. For Black households, it was $142,000. The average white household had about 7 times (~700%) as much wealth accumulated as the average Black family.

- For Hispanic families, their mean net worth was $166,000, with white households holding about 6 times (~600%) as much wealth.

- The Other group (which includes Asian, Pacific Islander, Native American, and others) had a net worth of about $657,000, which is “only” about 30% smaller than white households.

Clearly, past discrimination in housing, employment, and education has created long-term disparities.

What Can Help?

Given the history of racial discrimination in home buying and lending, various initiatives have been created to help increase homeownership for non-white families.

The Community Reinvestment Act of 1977 (CRA) was enacted in an effort to alleviate some of the past problems caused by racial discrimination in the housing market. The specific purpose of the legislation was to help low- and moderate-income households have easier access to credit to purchase homes. In this regard, it has at least moderately helped more families access lending services for home buying. However, there is acknowledgment that the CRA needs to be updated or modified to further encourage lending to disadvantaged groups.

Below are additional actions that have been or could be taken to improve access to homeownership:

- Federal agency involvement. The Department of Housing and Urban Development (HUD) has recently moved to improve access to homeownership by amending loan standards and increasing funding to down payment assistance programs. The Biden administration has also pushed various agencies to expand support for multifamily housing as well as manufactured housing.

- Private-sector initiatives. Bank of America has started the Community Affordable Loan Solution to help non-white families achieve homeownership. It focuses on zero down payment and zero closing cost mortgage loans. Wells Fargo also created an initiative called the WORTH (Wealth Opportunities Restored through Homeownership) program. It focuses on refinancing loans held by existing homeowners, particularly among Black households, to increase affordability.

- Home building adjustments. Ownership could be made more appealing by prioritizing the housing needs of different communities, including building more homes with multigenerational living as non-white families historically show a greater preference for this.

- Opportunity Zones. These are special designated areas created by the Tax Cuts and Jobs Act of 2017 to stimulate investment and development in low-income areas across the United States. These zones are relatively new, and, thus, the evidence on their impact is limited. There is the obvious impact that more money will be directed to these communities, but there is some argument that it may divert funding from other areas in need. It remains to be seen if these zones will move the needle on community investment and affordable housing.

- Additional legislative and policy changes. The Mortgage Bankers Association created a program called Building Generational Wealth Through Homeownership. This multifaceted program works on a variety of legislative efforts. One aspect has been a push for Special Purpose Credit Programs to encourage lending to underserved communities. Another initiative, which has seen some success, is to promote down payment assistance for minority borrowers.

Final Thoughts

As a result of the extensive history of discrimination in housing in the United States, there is significant room to improve non-white homeownership. We are already seeing this shift happen in real-time for some non-white individuals. For instance, in Taylor Morrison’s latest annual report, CEO Sheryl Palmer noted that over 60% of the company’s buyers in 2022 were Asian, Latino, and Black, up from less than 40% just two years ago.

As various government programs and private-sector initiatives continue to expand and grow, we hope access to homeownership will advance for all Americans. There’s both a business case and a human case for it.