The more than doubling of interest rates over the past 18 months has minimized the home buyer pool, but the impact on supply has been even greater. Consumers looking to move now, in what we are dubbing the “life happens” housing market, are met with limited options and high prices.

Builders have gained the upper hand in today’s housing market for three main reasons:

1. The ability to work with consumers. The impact of price cuts last year on the ‘fear of buying at the top’ mentality is well understood at this point. Now, prices are modestly rising at many new-home communities as supply remains limited. Our data at Zonda captures the persistence of incentives, though. The ability and willingness of builders to offer mortgage rate buydowns, funds toward closing costs, or flex dollars has been an imperative demand driver for the new-home market.

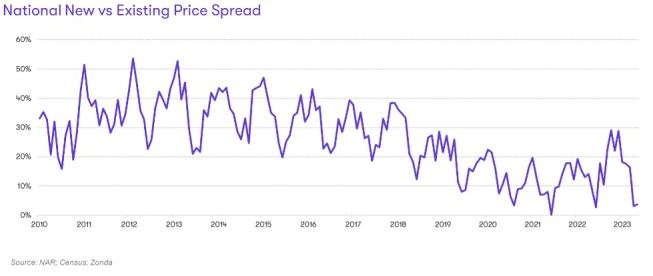

2. A shrinking price premium. New homes have traditionally been seen as luxury goods and, as such, they’ve been more expensive compared with the resale market. New-home prices averaged a 27% premium above resale prices dating back to 2010. The spread has narrowed to just 4% today. This likely overstates the trend as builders are intentionally trying to bring prices down by offering smaller homes or homes in farther away locations, but the shift is still significant.

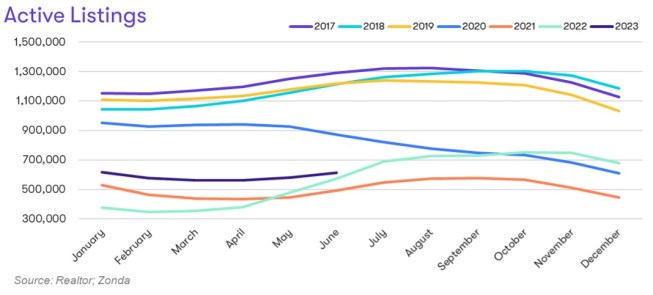

3. The biggest competitor has left the game. The existing-home market has largely frozen given the lock-in effect where existing homeowners are reluctant to sell and give up their current low interest rates. Estimates show 90% of homeowners have a mortgage rate under 5% and 60% have a rate below 4%. As a result, Realtor.com captured 614,000 active listings as of June, just over half the level seen during the same month in 2019.

Quick move-in (QMI) inventory from home builders has helped capture some of this demand as total levels are up year over year and compared with pre-pandemic times. QMI homes can typically be occupied within 90 days and serve as a new-home alternative to resale inventory. Builders now represent nearly 30% of total inventory compared with 10% to 15% historically.

While home builders have been able to benefit in today’s environment, the lack of resale inventory is causing dysfunction in the housing market. This dysfunction takes the form of housing payment-to-income levels severely out of whack in some markets and existing homes selling at elevated prices simply due to the lack of competition.

The supply and demand imbalance feels particularly intense today due to purchasing behaviors that became more prominent because of the pandemic. People buying investment properties, second homes, and vacation homes have tightened resale supply to an unprecedented level.

Policymakers are brainstorming fixes including exploring zoning reform to allow for additional home building, finding better uses for underutilized commercial space, and researching the efficacy of temporary or permanent changes to the tax code to encourage more selling or discourage investment properties.

More inventory is imperative to regaining health in the housing market. A viable path could come with a combination of increased housing starts hitting the market and more homeowners willing to sell once market interest rates fall closer to the levels seen over the past few years.

Higher inventory levels brought on by sellers that will also become buyers should have a net neutral impact on the market. We are, however, watching the supply that could be detrimental to the housing market. This supply would come from homeowners that become sellers without also becoming buyers. While a notable uptick is not in our base case, we are watching for any increase from:

- Investors offloading properties. During the height of the market, investors bought nearly 20% of all homes that were purchased. The share was even higher in Atlanta, Charlotte, Jacksonville, Las Vegas, and Phoenix where investors made up 28% to 33% of total transactions. These investment properties could be used as long-term rentals, short-term rentals such as an Airbnb, or could even be flipped. Investors that bought all cash or purchased at historically low interest rates have every incentive not to sell. If vacancy rates tick up, the financial assumptions used to justify the purchase don’t pan out, higher inflation pushes the cost of ownership too high, or the properties start to have negative cash flow, and the owners may find themselves in a place where they need to sell.

- Owners of second homes realizing they don’t use the property as much as anticipated. Demand for second homes increased dramatically during the pandemic. By August 2020, mortgage locks for second homes were nearly 90% above pre-pandemic levels. The pendulum has since swung in the other direction with March 2022 second home demand down nearly 53% since pre-pandemic. Those that bought a second home over the past few years may be perfectly content, but others may find they are not using the property as much as they anticipated or it may become a financial burden. A logical first step would be to convert the property to a rental, but as mentioned above, even an investment property isn’t a guarantee of financial success. A change in appetite first could be seen in Ocean City, New Jersey; Barnstable Town, Massachusetts; Naples-Marco Island, Florida; Salisbury, which stretches across Maryland and Delaware; and Flagstaff, Arizona, given the outsized share of second home purchases in these locations.

- Unemployment-related sales. The consensus among top economists and forecasting firms is that an anticipated slowdown in the economy over the next 12 months will be mild to moderate. This is supported by the Federal Reserve’s most recent Summary of Economic Projections that shows an anticipated rise in the unemployment rate from the current 3.6% today to 4.1% at the end of this year and 4.5% at the end of next year. This translates to nearly 750,000 fewer workers compared with today by the end of this year and roughly 1.5 million less by the end of next year. These individuals may or may not be homeowners and, if they are, there’s nothing to say they will be forced to sell, have a short sale, or go through a foreclosure. In fact, next to no one believes we are due for any kind of foreclosure crisis similar to the mid-2000s given the strength of the buyer over the past few years and the acquired equity. Even so, we are watching to see if any supply lift might accompany slower economic growth.

Demographic shifts, especially related to aging baby boomers, are another consideration that have more long-term implications on housing supply.

As mentioned, we don’t expect a rapid uptick in inventory without a notable change in the economy, market interest rates, policy, or demographics. We do, however, believe more inventory is needed to help address today’s housing affordability challenges. Policymakers will likely play a role in trying to alleviate the stress.

While the structural undersupply of housing is an important consideration in the new-home industry, once inventory rises, it will mean a loss of the competitive advantage for the new-home industry and an anticipated return to more ‘normal’ market conditions.