Demand is strong. But, many builders around the country tell us it’s shifting, throwing into flux a very basic calculus by which they make money.

This moment–where neither every new-home offering nor every submarket will meet with equal measures of success–means one of two things. You’ve either got to be better than most in paying for what you pay for, in your timing, and in your operational management. Or you’ve got to have a lot of money to hedge inevitable missteps, smooth out rough patches, and put timing on your side. If you’ve got one or the other–or better yet, both–the chances you’ll be able to play offense during this pivotal shift improve.

Here’s a way to look at it from the standpoint of three operational levers builders can and do manage, pace, price, and per-unit gross margins.

Monthly absorption rates–the number of sales per 30-day period–in each actively selling community indicate the pace.

Pricing serves three objectives:

- to level-set an absorption rate at a pace that pulls volume through at a sustainable margin

- to expand the margin and possibly cadence order growth at a construction-to-completion rate that meets volume goals, and

- to stimulate pace and pull through margins on increased volume

Because cost factors–mostly labor and materials–have gyrated wildly, and hit up against budget and operational model ceilings, passing all these costs along to the buyer has started to test home price tolerance levels, slowing the pace of absorptions, at least in some submarkets and certain product tiers.

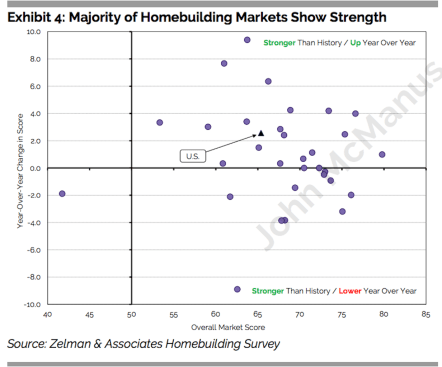

Here’s how the team at Zelman & Associates view the dynamic, with a forecast that suggests builders will be using all the levers they have at their disposal to keep sales pace and volumes where they need it to be. In the latest issue of The Z Report [which you can try for free by clicking here] notes:

On the pricing and margin front, results are more mixed. Given robust gains in recent quarters, pricing remains up sharply on a year-over-year basis, with our new home pricing index pointing to a 9.2% year-over-year increase on an apples-to-apples basis. However, this is down slightly from 9.3% in May and builders in our survey discussed being more cautious on pushing incremental increases given affordability concerns in some markets and softer absorption growth of late. Meanwhile, cost inflation continues to creep higher, with material and labor cost inflation increasing to 5.1% year over year from 4.9% in May and reaching the highest level in five years. While price appreciation remains sufficient to offset cost pressures for the time being, the spread between pricing gains and cost inflation continues to compress.

Builders’ natural reflex is to hyper-focus on cost management, to “sweat the little stuff,” and to capture improvement by releasing productivity traps within their own systems, structures, and processes.

And well they should be keen to rid operational processes of time, materials, and labor that contribute little or no ultimate value to consumers, to trade partners, to stakeholders, and to the company itself.

As costs for skilled labor and commodities get wrapped around the axle of volatility the models to preserve, grow, or mitigate loss of margins get trickier and trickier minus a factor that would contain the negative impact of one or both of those areas, which is why the discussion of and capital investment in offsite factory construction have gained such momentum in the past 24 months. A fundamental question emerges in such an environment: Is operational excellence more about the ability to take costs out, or the capacity to generate value disproportionate to expense?

Smart, and in many cases, bigger, more well-heeled organizations have begun to look beyond the usual-suspect opportunity-areas for process improvement that can lead to reduce costs. They’re looking at distances and deltas of money and time locked up in common practices like commissions to local real estate agents, and other marketing and sales functions, bringing data to bear in how their value stream can flow strong and uninterrupted between themselves and potential buyers.

Here’s what we expect in the six-to-30 months ahead.

- More volatility on direct input costs.

- More volume, with greater emphasis on entry-level buyers.

- More challenge to margins.

- More advantage to bigger players who can look at margin compression as an opportunity to drive greater value directly to home buyers.

- More mergers and acquisitions.