Renting by choice, one of the past decade’s “stealth” macro consumer and housing preference trends, has shown the kind of staying power and scalability that’s got all the big single-family for-sale home builders abuzz about the strategic opportunities ahead.

One of those big players, Toll Brothers, last week made public a deep and far-reaching commitment in the space that we had reported was near-ready-to-announce this past December, a $60 million investment in a $400 million venture that aims to iterate a successful build-to-rent BB Living business model from its base in Phoenix to Denver, Las Vegas, Jacksonville, Dallas, Houston and Boise markets.

In last week’s 2nd Quarter earnings call with Wall Street investment analysts, Toll chairman and ceo Doug Yearley spoke of great expectations and clear alignment with Toll’s product offerings, geographies, and current customer segmentation road-map. From a transcript of the call, here’s Yearley’s commentary:

Doug Yearley

Doug Yearley. Credit: Noah Kalina

We are also investing in the single-family build-to-rent sector. This is another business we believe has great potential. This quarter, we formed a joint venture with BB Living, an established build-to-rent developer and a large financial partner in a $400 million joint venture to purposely build and operate single-family rental communities. We are initially targeting the Phoenix, Denver, Las Vegas, Jacksonville, Dallas, Houston and Boise markets. While Toll Brothers has committed a relatively modest $60 million to this partnership, we believe this investment will produce strong returns over time. It’s viewed as an ancillary income stream. We see this as more and more renters may prefer to raise a family or live in a single-family home versus a apartment complex or community or building. And so it is part of our Apartment Living group.

The venture will be marketed as BB Living. It will not be branded Toll Brothers. Our role is as financial partner, but also [to offer] parental supervision of operations. We will be looking at land opportunities because it’s in markets that we are in. We will be helping with architecture. We will be helping with construction. BB will play the lead role when it comes to management and lease up. The locations are primarily in masterplanned communities — large masterplanned communities — that have a wide variety of price points and products now, and the master plan developers are excited to bring in a single-family or townhome product that looks the same as many of the other builders — the for-sale builder’s products. It’ll just happen to be a rental. The buyer demographic is primarily younger families that, as I said, want to rent, but they want to raise a family, want a rent in a home and BB Living has had great success before us in Phoenix. We will now be joining them for future opportunities in Phoenix and expanding their operation into the markets I mentioned earlier.

As we noted previously, this is the first and biggest, but by no means the last we’ll see, hear, and report of strategic commitments by for-sale home builders in the single-family built for rent space. Just about two weeks ago, Clayton Homes ceo Kevin Clayton mentioned that the nation’s largest builder and distributor of manufactured homes and, now, a top 15-ranked site-build operator, is piloting build-for-rent home communities within some of its massive geographical footprint.

Fundamental demand for single-family for-rent taps two robust–and growing–well-springs of household economics these days, one being the rent-by-necessity group of mostly younger families for whom down payment hurdles, monthly payment challenges, interest rate pressures, and rising for-sale prices have put homeownership beyond their means, at least temporarily.

The other group, whose magnitude and clout are on an upward trajectory, are households who could afford to buy, but choose to rent–opting for the flexibility, the simplicity, the relatively bother-free, “less strings-attached” lifestyle that not owning lends–and, yet, want to do so in a detached, single-family house in a new residential community.

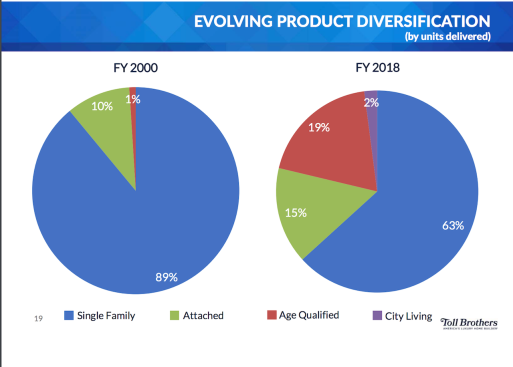

Toll Brothers housing-type diversification trends.

As Yearley notes, this group wants to rent, but prefers doing so in horizontal neighborhoods rather than vertical apartment communities. Now, Toll adds to its array of offerings in almost every imaginable housing preference type and every real estate location and community format.

A number of big builders are already producing some of their new-home stock for purposes of supplying single-family rental property management enterprises that emerged in the wake of the foreclosure crisis and gained traction as a real estate asset class by amassing cheaply-acquired distressed properties and leveraging technology to manage them as rentals. Meanwhile, the urban higher-end and luxury apartment market took off during those same years, starting early on in during the economic recovery. The rapid uptake, particularly for the Class A, highly amenitized, and luxuriously finished apartments in more and more major urban areas exposed a heretofore un-pronounced and now-expanding marketplace of renters by preference: those who could buy, but choose to rent.

According to National Multifamily Housing Council data, 15 million households, representing 35% of renting households, rent single-family homes rather than multi-unit apartments. Also, one of every four renters of properties newer than 1990 earn household incomes of $75,000 or more.

Masterplanned communities, increasingly, have begun allocating community tracts specifically for single-family rentals, and some actually integrate for-sale and for-rent new properties in the same neighborhoods. Often, although finished vacant lots are scarce and land prices are high and regulation-laden everywhere, suburban masterplanned communities offer a lower-cost alternative to urban and infill land expense.

With demand on the rise for rentals, and Millennials reaching a now-or-never moment in family formations, single-family rental taps into competencies production builders have around leveraging relationships with master planners, relatively fast construction cycles, and established community management and programming infrastructure, all of which contribute to faster access to cash-flow than high-rise and other attached product offerings allow.

Advancing technologies and lower barriers to entry on property management systems and resources allow traditional single-family for-sale players to pivot, and more of them are doing so. Strategic commitment, investment, and emphasis on single-family built-for-rent will likely pivot from low single-digits of housing activity volume into a relatively small-but-solid double-digit percentage of homes over the next 10-year time frame.