For D.R. Horton, the once and would-be future No. 1 home builder in America, the business of home building may not be easy, but it’s pretty simple.

Build houses and neighborhoods people say they want, and sell them at prices people in those locations can pay.

Rinse. Repeat. Win.

There’s a lot of talk, including a lot of talk among builders, about costs right now, and how costs’ impacts on house prices could subdue demand and bring this recovery cycle to a grinding halt as the good part—an entry-level surge—has been just getting going.

From Horton, which together with Lennar, currently accounts for about one of every five new homes being sold in the U.S. right now, the talk-track keeps it simple.

Here’s Horton VP of Investor Relations and Communications Jessica L. Hansen responding during the company’s most recent (July 26, Seeking Alpha) earnings call, as investment analysts sought to detect a signal vs. the noise of air pockets, slow-downs, and a deceleration in order pace as rising costs and rising interest rates buffered the market.

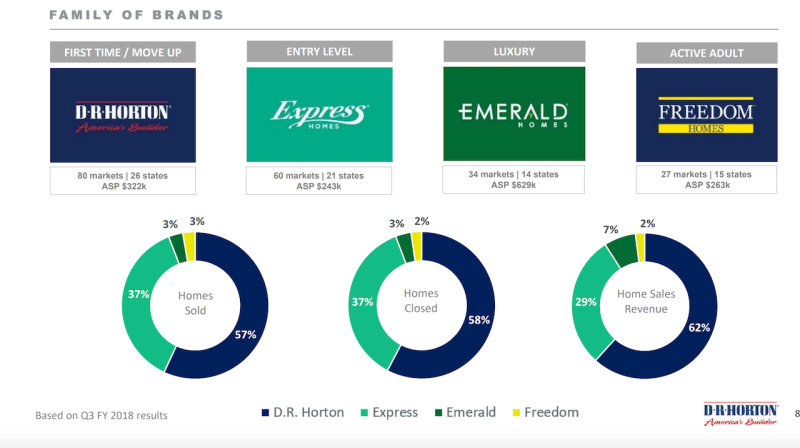

For the quarter, we saw a typical seasonality. So we saw a very strong demand as we moved throughout the quarter and just typical seasonality as we moved into the early summertime. We do believe that our outperformance as it pertains to our sales really is because of our positioning and our product offerings across the country. If you look at our results this quarter, it’ll be posted in our supplementary data after the call, but Express was 37% of our sales and closings and our new Freedom brand is now 3% of our sales. So those are very affordable product offerings that we are very focused on keeping affordable. So there’s still extremely limited supply at affordable price points. And so where we can get that product on the ground, we continue to see very robust demand and no sign of weakness at those price points. So I think that’s the main reason that’s differentiating us when you look at our sales versus some of the others out there in the industry today.

And the fact is, D.R. Horton is among the best–itself, NVR, and Lennar–at the “where we can get that product on the ground” part of the equation, thanks, as Hansen says, to its “positioning and product offerings.”

Notes from Cleveland Research analyst and partner Omarr Aleem are telling in light of Horton’s sense of its own plan, agenda, and ability to execute versus the clamor of media and expert commentary that points to a structural slowdown in the new home market.

Here verbatim is a bullet-point roster of notes that Aleem and his Cleveland Research team came away with after meetings with D.R. Horton executive management:

Express

- We expected Express growth to limit margin at some point

- We haven’t seen it–margin has been stable to better than the average

- If there is more competition in that segment, could limit margin

- We can’t meet demand in Express communities

- We have had less competition than expected in Express format homes

- Our spec strategy and philosophy help us here – D.R. Horton is 75% spec versus market at maybe 25%

- Other builders don’t want to build spec

- Spec strategy puts us in competition with existing homes

- First-time buyer doesn’t want to wait 6 months for a home to be built/delivered

- Lack of capital for builders has limited competition

- D.R. Horton is working to keep Express homes affordable

- Taking footprint down a bit and putting in fewer amenities (take out granite in master bath, for instance)

- We are engineering costs out to manage this

- First-time buyers are focused on monthly payment

- D.R. Horton is making that payment more affordable

- If customers want to buy less house, D.R. Horton will have fewer floor plans

- A 4-bedroom, 1,800 sq/ft ranch is the house people want We will not abandon move up, but that isn’t central to our strategy

Freedom

- Freedom is adding to growth, but is not a big piece of growth expectation

New Home Prices

- D.R. Horton ASP is $300k and growing like everyone else

- The key is that D.R. Horton has more first-time product

- The new home premium is 15-20%

- But there’s no not a lot of housing stock to compare it to

- The key for home buyers is the monthly payment

- With sub-4% rates, owning is cheaper than renting

- At current levels, the two are very competitive

Margin

- We have achieved better margin on strong demand and increased buying power

- The expectation has been better margins for three years

- We will continue to sell homes no matter the margin

- At this point, we expect to sustain the higher margin

- Our internal focus has shifted away from margin and to returns

- The key is maintain pace in the community

- Sometimes absorption/pace will increase even when demand slows We also talk about pretax margin versus gross margin

Gross Margin

- Gross margin is not going back to where it was in the last upcycle

- That was driven by loose credit

- Land-light strategy will limit margin upside a bit because we have to pay a premium to purchase a finished lot

- We don’t want to speculate with land during this cycle

- We will buy when land prices roll over

Mortgages

- Change in rates not changing buyers at this time

- Higher mortgage rates are not a material damper on demand

- Locations and size and features are what determine the success of the community

- We did see impact the last time rates spiked

- Mortgage rate up 100bps in a few weeks spells trouble

- This time the change in rates is more gradual

- When affordability is an issue, customers will buy less home – they know/watch the monthly payment

- FICO trend is still quite good FHA loans are down 10 points within our mix

Costs

- The spec strategy can be helpful in an inflationary market – know cost before set price

- Lumber is 8-10% of the cost of a home, should be a benefit looking into 2019 We buy lumber on a 13-week trailing average basis

- We have seen material and labor costs tougher

- National supply deals have limited input costs, offsetting with volume rebates

- We feel a bit better on labor

- Simplifying Horton/move-up product is helping

- More construction jobs are getting added

- Build times have not changed for D.R. Horton. Our product offering is helping with this.

- We have been able to offset these pressures with pricing

- Costs are likely worse for the next quarter or two, then will begin moderating

- We can keep raising price to offset 2-3% annual cost inflation

- Consistency in product and labor needs unlocks margin in this business

- Coming off the next peak, we can reset labor and materials costs and de-spec houses

Next Downturn

- The next recession won’t be like the last one for housing

- Next round of baby boomer demand is coming

- Millennials will be forming households

- There is demand coming

Biggest Worry?

- Our ability to build affordable quality product

- More square feet and less cost

- How do we control labor?

- How do we change product offering?

- Labor has been the bigger driver of inflation

- We have recently heard some easing of labor inflation – not as broad or bad as a year ago

- D.R. Horton has some leverage with labor by adjusting the build process

The striking thing about this series of comments, observations, and assertions? Recognition and accountability for what D.R. Horton and its leadership team are accountable for irrespective of external circumstances, conditions, or shifts. That difference alone sets the Horton team apart from most of the rest.