THE MANUFACTURED home industry accepts boom and bust cycles, in the same way the people of Southeast Asia accept monsoons and flooding. Both groups maintain a certainty that one day the rains will cease, and they will begin the familiar rituals: burying the dead, cleaning up the mud, and rebuilding.

But in the last couple years, the “monsoon” of bad news hitting manufactured home builders has been especially devastating. Fates have conspired against them, it seems.

First came the usual practice of lenders exposing the manufactured industry to far too much risk. Given the low federal lending rate, they apparently just couldn’t resist passing those rates on to people who could barely make ends meet. Widespread bankruptcies ensued. Lenders lost their shirts. Owners lost their homes.

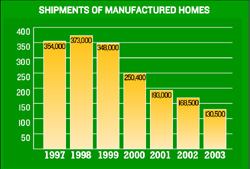

“We peaked out in 1999,” recalls Jim Newman, CEO of privately held Manufactured Housing Enterprises (MHE) in Bryan, Ohio. “Now we’re half the size we were then.” The company dropped from 1,360 homes in 2002 to 972 homes in 2003.

Along with the lending mistakes, says Newman, this prolonged period of low interest rates has hammered the manufactured housing industry. Jim Clifton, with the Manufactured Housing Institute in Arlington, Va., explains, “These rates, the lowest in 30 years, have created one of our biggest challenges. One of our key markets, renters, can now afford to buy a site-built home with very little money down.”

Shaking The Past What’s more, Clifton says, the industry is still fighting an uphill battle with public perception. “The public’s view of us [as low-quality, mobile homes] is about 30 years behind the reality on the ground,” he says. “That image is based on the existing stock of 11 million homes, many of them metal-covered, single-wide … product.”

Today’s product, he says, has heavier framing, thicker drywall, and better quality control throughout. He adds that the industry has been pushing hard (so far with limited success) to encourage code officials to accept a version of manufactured home that meets the Energy Star requirements. That would give a much needed credibility boost to the industry, he says, and make the homes more highly competitive in their price point.

Course Corrections Whatever the ultimate outcome of the Energy Star initiatives, says Clifton, the industry’s rock-bottom experiences have shaken it to its stubborn core. There have been a few pleasant surprises in recent months, however—such as when billionaire Warren Buffet purchased top manufactured housing producer Clayton Homes. “That really turned around the whole feeling in the industry and gave everybody hope,” says Clifton.

Fannie Mae’s recent announcement that it will create a lending program for manufactured homes also should have a positive effect on the challenged industry, by raising qualification standards, limiting equity borrowing, and requiring slightly larger down payments.

“The Fannie Mae entry has been a big confidence builder,” Clifton says. “One of their key partnerships is with GMAC, one of the world’s largest mortgage holders.”

Eager to please these new bankers, the industry has become more proactive with smaller lenders, Clifton says, in an effort to prevent future melt-downs of this magnitude. “We have a program called ‘Lender Best Practices,’ which is like a Good Housekeeping Seal of Approval for lenders.”

Another program that should lower the bankruptcy rate is the Mortgage Asset Research Institute (MARI) fraud reporting system, which helps track developers and home buyers who use fraudulent documents or statements to bilk the lending system.

Hedging Bets Lending for manufactured homes is expected to increase by 33 percent this year, thanks to Fannie Mae’s program, although sales will lag far behind that number for a while. At the same time, some companies have taken refuge in the growing modular market.

Jim Newman of MHE, for example, says his modular product has taken off in recent months. Indeed, whereas manufactured housing slipped by 50 percent for many companies, modular units from Westchester Modular of Wingdale, N.Y., and Muncy Homes of Muncy, Pa., managed to grow by about 10 percent.

“We’re attracting a lot of interest from site builders,” Newman says. “They’re realizing that we can build a house for $33 a foot, and we’re doing 2,500-square-foot houses. Builders are dealing with a lot of uncontrollable labor issues right now. So we can provide a solution.”

Lenders Fight Fraud Defaults on loans have severely damaged the manufactured housing industry, resulting in thousands of foreclosures—and, to make matters worse, banks are becoming ever more cautious about lending, thanks to a rise in fraudulent activity.

Ever heard of mortgage fraud? One negative side effect of ultra-low interest rates has been a rise in the number of people defrauding borrowers and lenders out of their money by lying about real estate values. A common fraud scheme: Buy a low-cost home, then sell it for quadruple the price to an unsuspecting person by faking the appraised value. Mortgage Bankers Association of Washington held a conference recently to discuss the perils fraud poses to lenders. Here are a few key points.

Source: Mortgage Bankers Association