WASHINGTON (May 12, 2016) – Inventory shortages and rising prices notwithstanding, the Realtors meeting here this week see 2016 as the best year for home sales since 2006.

Lawrence Yun, chief economist of the National Association of Realtors, presented his midyear economic and housing forecast at the 2016 REALTORS® Legislative Meetings & Trade Expo here, flanked by U.S. Sen. Elizabeth Warren (D-Mass.), who delivered remarks about how student loan debt is weighing on young adults, the housing market and the overall U.S. economy. According to Yun, monthly existing-home sales were uneven in the first quarter but still came in at a seasonally adjusted annual rate slightly higher (5.29 million) than last year’s overall annual pace (5.26 million). Demand has mostly remained strong – especially in the top job-producing metro areas – and is being upheld by mortgage rates near three-year lows and the 14 million jobs gained since 2010.

“The housing market continues to expand at a moderate pace in spite of the fact that home prices are rising too fast in some areas because of insufficient supply fueled by the grossly inadequate number of new single-family homes being constructed,” said Yun. “The good news is that pending sales in recent months have remained stable and should support a modest gain in home sales heading into the summer.”

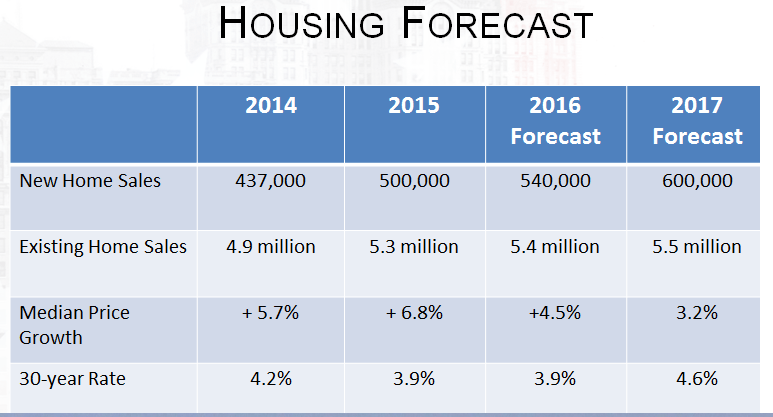

Yun’s forecast projects existing sales to finish 2016 at a pace of around 5.40 million – the best year since 2006 (6.48 million). Prices should end the year up between 4% and 5%, a slowdown from last year’s torrid 6.8% pace.

Yun said the ongoing absence of first-time home buyers is the missing link to a full housing recovery. Job growth has been strong for multiple years, rents have soared in many areas and mortgage rates are historically low, he said. But rising home prices, flat wage growth, the lack of available starter homes and repaying student loan debt is thwarting many young would-be buyers.

“Spectacularly low mortgage rates mean today’s prospective home buyers are the luckiest in a generation but the unluckiest in actually becoming homeowners because of the roadblocks hampering their ability to buy,” said Yun.

Turning to his forecast, Yun said that although contract signings nationally have held steady for several consecutive months, regional differences are beginning to appear in places where home prices have appreciated the fastest – specifically in parts of the South and in the West. Although data from the Realtors Confidence Index shows that home buyer traffic is still strong, demand is somewhat weakening from a lack of available inventory and the subsequent affordability pressures it’s putting on a large segment of would-be buyers.

Again, Yun appealed to the home building industry. “Home builders need to significantly ramp up production so that more existing homeowners can trade-up and list their home for sale. Otherwise, inventory shortages will continue and demand could soften even more in some areas as a greater number of buyers are unable to find homes at affordable prices.

Yun foresees housing starts ending up higher than last year (1.1 million), but still below the 1.5 million necessary each year to keep up with current demand. New home sales are likely to total 540,000 this year, which is only a little more than half the rate from the pre-boom years in the early 2000s.

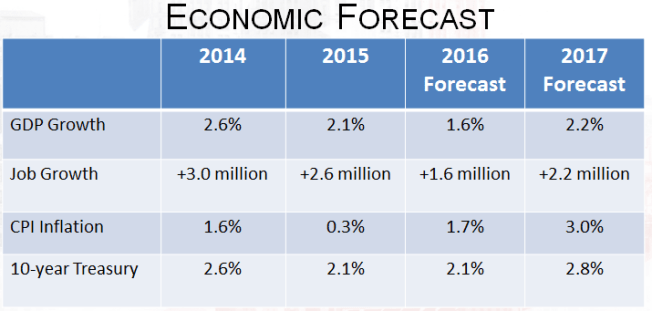

Yun said rents, which rose last year at a seven-year high, will be a big driver of future inflation, along with gas prices, and will ultimately steer the direction of mortgage rates. If rent growth continues at its current pace, inflation will be stronger and push rates higher. Slowing rent growth would have the opposite effect by keeping a lid on inflation and holding rates at a very manageable level. For now, he foresees mortgage rates continuing to hover around 4% in coming months before gradually moving upward into next year.

Despite solid job gains in the past few years, Yun said that economic growth continues to be unimpressive. The rising U.S. dollar against other foreign currencies and the slowing global economy since late last year would likely be causing our economy to teeter on the edge of a recession if it weren’t for the boost from the housing component of Gross Domestic Product. Through the rest of the year, he expects GDP to register at only 1.6% and be primarily kept afloat by housing and consumer spending.

Even with underlying challenges, Yun explained that the housing market has come a long way since the depths of the recession. Mortgage delinquency rates – especially for Veteran Affairs mortgages – have subsided to near pre-crisis levels and home prices have rebounded substantially in a majority of metro areas, which in turn has boosted household wealth for many homeowners.

“The economy should still expand enough to continue the current pace of job creation, which will in turn lead to slow, but steady sales gains for the housing market,” concluded Yun.