During the housing recession, Ed Sullivan, chief economist for the Portland Cement Association (PCA), was one of the few consistently bearish prognosticators. He resisted joining many of his brethren who perennially saw a recovery just around the corner. For years, Sullivan’s projections about housing starts and sales were reliably conservative.

So one indicator that the housing market is on the mend for real could be PCA’s more upbeat assessment of market conditions as a platform for future growth. “The only way builders make money is if prices rise and inventories are low,” Sullivan says. “Those conditions have been met.” He also has changed his tune about the impact of foreclosures, and now believes there will be “a muted, slowly spread-out release of these homes” by banks and investors.

Sullivan expects pent-up demand, which he estimates at 6.2 million potential buyers, to “leak out gradually” over the next two to three years, while an improving economy creates new demand “for the next three to four years. Those are big pluses.”

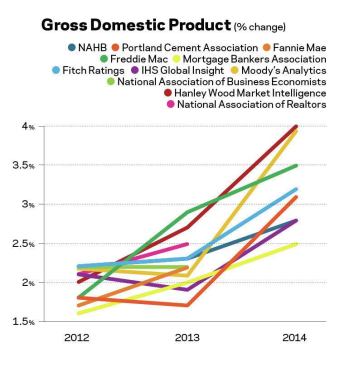

With his predictions, Sullivan joins the majority of economists and researchers that sees what Frank Nothaft, Freddie Mac’s chief economist, calls a “healing” housing market, one that could boost the nation’s Gross Domestic Product by a half percentage point in 2013. “Housing already matters,” asserts Brad Hunter, Metrostudy’s chief economist.

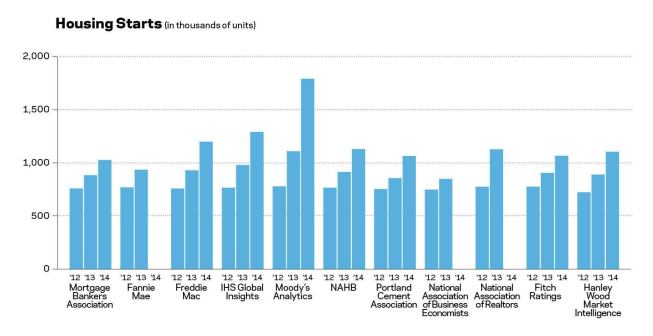

Unlike in past years when forecasters regularly overshot the market’s actual performance, housing is outrunning most recovery predictions. The Census Bureau’s Residential Construction report for November pegged annualized housing starts at 861,000 units, a number that far exceeded even the most optimistic forecast for 2012. Whether this starts rate holds up over the remainder of the year remains to be seen. But most economists now feel confident that housing is poised for significant gains through 2014 at least.

“All of the drivers are in place,” says Patrick Newport, director of long-term forecasting at IHS Global Insight. “Inventory is at a seven-year low, and interest rates remain low, which is one reason why prices are rising. The only thing that would slow down the housing recovery would be another recession.”

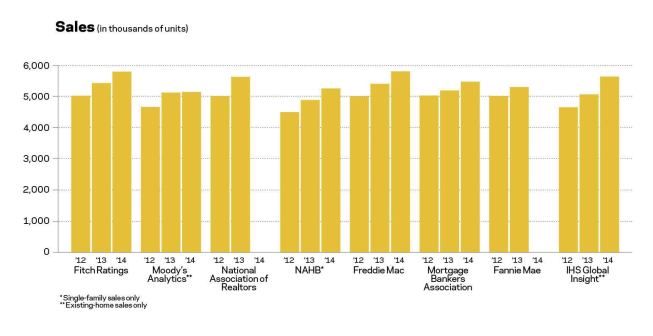

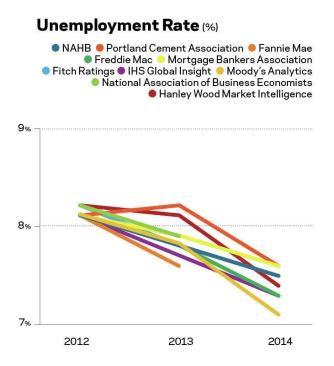

Ah, but there’s the rub. Can housing’s recovery continue despite what most economists foresee as only modest improvements in the overall economy and employment (see charts) over the next two years? The October Census numbers for annualized new-home sales, which fell by 3 percent to 368,000 units, didn’t inspire confidence that buyer demand was back in force, either. “Everything we see [in housing] indicates we’re on a positive track,” says Gary Painter, director of research for the Lusk Center for Real Estate at the University of Southern California. But, he adds, “It all comes down to fundamentals: household formation and income growth.” Painter cautions that different markets will improve at different rates, and places that don’t have rapid job creation will lag.

Any ambivalence on the part of forecasters was partly due to their uncertainty about the ability of Congress and the White House to prevent the economy from tumbling over the so-called fiscal cliff, which if left unresolved on Jan. 1, 2013, would automatically trigger more than $7 trillion in tax increases and spending cuts over the next decade. In early December, when this article was being prepared, no deal was in place. “If we can get past the fiscal cliff, there should be modest to average growth in 2013. But that’s a big if,” says Ken Simonson, chief economist for Associated General Contractors of America and president of the National Association of Business Economists.

“One way or the other, the fiscal cliff will be addressed,” added Bob Curran, managing director with Fitch Ratings, in late November. “If the results are higher taxes and fewer entitlements, I can’t see how that can be good for economic growth. In fact, housing might actually be more of a help to the economy than the other way around.” Fitch expects housing starts to rise by about 28 percent next year, and home sales to increase by nearly 10 percent.

It’s worth noting, though, that more than a few economists are still gauging the housing recovery based on pre-recession market conditions that, arguably, might never occur again. Nothaft, for example, noted on Nov. 14 that while home prices over the previous 12 months had risen 12 percent, “we’re still far from a healthy pace of housing activity,” which in his mind would be 1.8 million starts, a number Nothaft doesn’t think will be achieved for at least four or five more years.

Trulia’s “housing barometer” for November stood at 51 percent, which meant the real-estate site considered the housing market just halfway recovered. Jed Kolko, Trulia’s chief economist, expects his barometer to be in the 90s by 2015 or 2016, “but even then, some spots could still be soft,” he says.

WORRYING ABOUT LOTS AND LABOR

The strength and pace of housing’s recovery hinge on how many buyers feel comfortable about getting back into the market, and when. Policy decisions that affect those buyers’ finances and stability will definitely influence whatever outcomes occur. And Jason Gold, a senior fellow with the Progressive Policy Institute, predicts that housing will play “a significant role” in President Barack Obama’s second term.

Writing in U.S. News & World Report, Gold expects Democrats to reintroduce refinancing initiatives that include mortgage principal reductions. New rules on consumer protection and lending—including the Qualified Residential Mortgage, which will regulate lenders’ capital requirements—are scheduled to be announced this month. The government’s long-term investment in Fannie Mae, Freddie Mac, and the Federal Housing Administration—which currently guarantee 90 percent of all new mortgages—should move to the front burner in Congress in 2013. And can the popular mortgage interest deduction survive Congress’ budget knife?

“We worry about how the deficit/debt reduction efforts will work out, what kind of tax reform we will get, and how well the rest of the world economy performs,” says David Crowe, NAHB’s chief economist.

Many of these factors are beyond builders’ control, of course. So Crowe and other economists take solace in signs that household formations have picked up, and house price trends have been positive. (The NAHB, for example, is calling for a 23 percent increase in new single-family sales in 2013, and a 33.8 percent increase in 2014.)

Still, industry watchers are keeping a close eye on potential headwinds that could impede housing’s forward momentum. First and foremost is whether credit for home buyers and builders will be available in sufficient amounts. Two other bumps in the recovery road could be the impending scarcity of finished lots and the difficulty of finding skilled jobsite labor.

As of early December, lot shortages were mostly localized, Crowe says. “They are scattered enough to believe they are not serious enough to affect the national forecast.” In fact, Crowe suggests that the housing recession has allowed the industry time to “rebuild the infrastructure by starting new pipelines of developed lots.”

Other economists see lot shortages as a more pressing issue. In a Nov. 15 interview with Bloomberg TV, Metrostudy’s Hunter estimated that there was only a 16-month supply of finished lots “where builders want to build.” And choice lots “are dwindling fast.” Hunter added that Metrostudy’s projections for 890,000 home starts in 2013 would have been closer to 940,000 were it not for lot shortages nationwide.

As for labor, manpower shortages are not widespread yet. But Simonson notes that the construction industry’s workforce, which peaked at 7.7 million in April 2006, is still down 2.1 million, and shrank by 500,000 in the past two years alone. “Construction employment has not been growing steadily, and it’s a problem getting people to come into this field.” Jonathan Dienhart, director of published research for Hanley Wood Market Intelligence, says a diminished labor and supply chain will require capital outlays and time to expand. “So there may be some growing pains trying to ramp up again.” And if buyer demand broadens nationally, “all of these housing-start projections would be pie in the sky,” says Curran of Fitch Ratings.

RUSH FOR RENTALS

Perhaps the biggest question mark about housing’s future is whether rising demand for rental options is permanent or transitory.

Foreclosures certainly have abetted the surge toward rental, as investment groups such as Blackstone, Colony Capital, and Carrington Mortgage Services gobble up foreclosed homes aggressively and convert them to rental properties. Even as foreclosure activity abates, “you still have about 10 million owners underwater and another five million who are behind in their payments,” observes IHS’ Newport. “A lot of these people are going to lose their homes eventually and won’t be able to buy. So trends of lower homeownership are pretty inevitable.”

More builders seem to want in on the rental trend, too. Construction of buildings with five or more housing units was up nearly 63 percent through the first 10 months of 2012, according to Census estimates, compared with a 35 percent jump in single-family starts. The ratio of annualized multifamily starts to single-family starts during this period was just under 1:2.

Yet, despite growing demand for rental, Simonson sees single-family construction “rebounding strongly,” a view that other economists share. As rents rise, ownership will come back into vogue, they say, especially as Millennial-age buyers get married and have children.

A full-blown recovery in the home building sector—whatever that turns out to be—might be years away. And there are plenty of factors, some of them possibly unforeseen, that could slow housing down. But the market is undeniably moving in the right direction. And as long as the economy doesn’t tank again, this time the forecasters actually could be right.