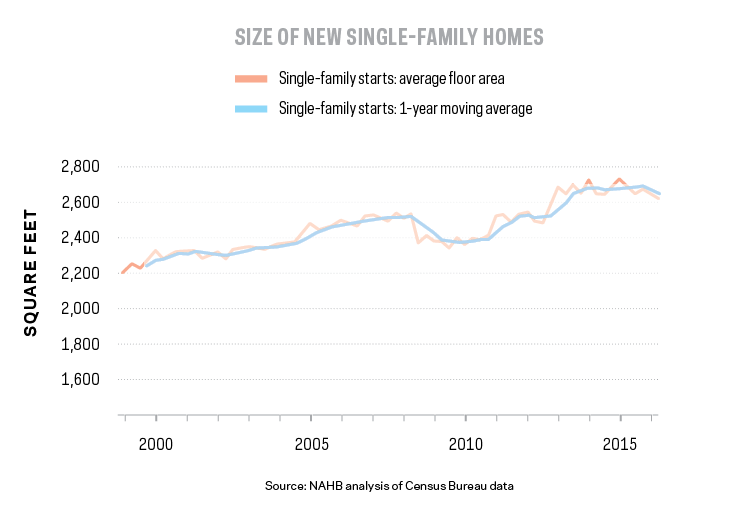

One defining market dynamic of the post-recession period has been the shift to larger, more expensive new homes. This marked a rebound after the housing downturn. Due to reduced housing demand and policy effects from the first-time home buyer tax credit, average new-home size fell during the Great Recession. Home size reached a low point at the start of 2010.

On a one-year moving average basis, average new-home size was approximately 2,370 square feet for the first quarter of 2010, according to NAHB analysis of Census Bureau data. After the start of 2010, however, home size grew as home builders increasingly shifted to larger, more expensive homes. This made economic sense, particularly during a period of rising regulatory burdens and costs, as demand was more robust at the high end of the market during this period.

As a result, average home size grew by more than 13% to 2,683 square feet by the start of 2014. At the same time, the difference between median new-home prices and median existing-home prices expanded. In 2010, that gap was about $48,000. By 2014, it had grown to more than $76,000.

However, a couple of market changes have since taken place. First, over the course of 2014 and 2015, the growth of new-home size stopped. This marked the end of the market shift to the high end. Second, since the end of 2015, average new-home size has fallen. For the fourth quarter of 2015, on a one-year moving average basis, average new-home size stood at 2,691 square feet. By the end of 2016, it had fallen 2% to 2,635 square feet.

Typical new-home size remains larger than just a few years ago. Nonetheless, this (small) decline is consistent with an overall broadening of new-home inventory being offered by builders, with more entry-level homes and townhouses being constructed to meet growing and unmet demand at the lower end of the market. During this same period, there has been a slight closing of the price gap as well, with January 2017 data indicating a difference between new and existing median home prices of $71,000.

The question for the marketplace is whether additional declines in size and price will take place in the quarters ahead. As interest rates rise, higher priced homes will face comparatively weaker demand. And as labor, lot, and building material prices grow, builders will need to efficiently manage costs to make sure new homes remain competitive. There are clearly positive conditions for builders given ongoing tight existing-home inventory, but a broadening of the inventory base is good news for home buyers and the building industry.