One of the things you’re not reading a whole lot about in BUILDER these days?

Start-ups.

Let me get this straight, and in so doing kidnap one of my dad’s favorite sayings to us as kids. So, builders don’t grow on trees?

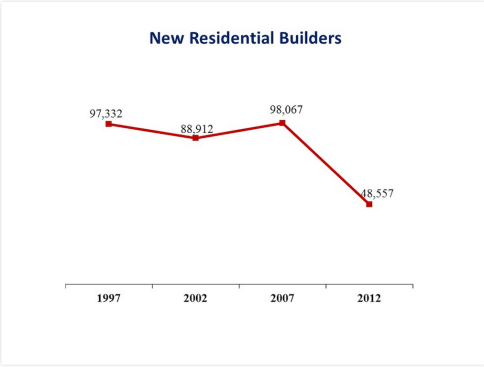

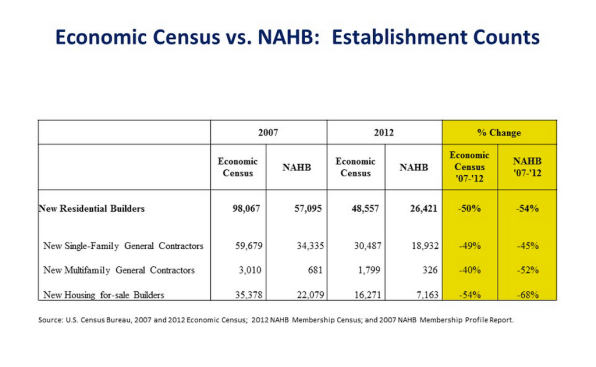

Yesterday, National Association of Home Builders economics researcher Rose Quint lit on an astonishing piece of data from the Census Bureau’s Economic Census that, as dramatic as it is, confirmed what we know. The Recession of 2007 to 2011 annihilated home builders. Here, from the data source itself, the picture of that stark reality in a fever chart.

Now, one thing to keep in mind is that the years 2011 and 2012 probably marked the worst of the worst of the aftershock and great freeze effects of the downturn. By 2013, the first leg of the recovery was well underway, and the Economic Census data, once it’s available for 2013 and 2014, will probably show a couple of feisty strides in a positive direction. Still, let’s hold that thought for a moment, and look back at what Rose Quint’s analysis tells us.

It says that the decimation in lending, spending, owning, developing, and building homes during the down years put half the companies in business in new residential construction out of business. The NAHB’s own membership rolls reflect the same sorry story.

So, answer me these question. Were there too many builders and building companies during the 1997 to 2007 decade? Or are there too few now? Were the go-go days of hiring anybody who could fog a mirror normal? Or, are the no-no days of hand-wringing about how to find just one more solid, skilled talent resource normal?

No doubt, off-shoring, outsourcing, and technology in the form of data science, machine learning, robotics, and process simplification account for some of the head-count reductions. What percentage might that be? How many more people, and companies, and investment dollars are the right amount?

Builders don’t grow on trees, because it’s risky to become one. It’s risky to go into a business that assumes an outsized amount of upfront capital and time investment on deals that may or may not play out as planned. We ask that (huge upfront risk against heavy odds and lots of regulatory drag) of individuals, and we ask it of companies.

The Wall Street Journal’s Nick Timiraos as much as points a blaming finger at large, capital-rich multiregional home building enterprises for the glacial, thumb-twiddling, watching-paint-dry pace of housing’s recovery.

Of course, there’s a lot of factual accuracy in Timiraos’ “Has Industry Consolidation Held Back Home Construction?” piece, and he is one of the better mainstream press reporters on the industry. Still, how can he reach this conclusion?

In home building, the survivors have been much less willing to take the risk of buying land and building developments in more-distant suburbs.

In how many ways is there an entirely off-base, unhelpful, if not false, ring to that observation?

To infer that the people who invest capital and time and other resources in any venture would say, “ok, let’s start putting our resources where there’s no sign of economic activity, diametrically opposite of what job formation, industry activity, age segmentation, etc. would suggest we do…” or “all the data says that closer-in, jobs-centric, higher-end communities are where the money is, but let’s not do that…”

In a backwards sort of way, Timiraos’ thesis may veil a truth.

Which is this. Local regulators, local interest groups, local, regional, and lenders and investors, etc. have spoken loud and clear in the first part of the recovery. They want “haves” home buyers, and “haves” home building companies with deep pockets, and “haves” new communities to cushion their own risks. The economy, society, even culture has been risk averse, perhaps with due cause.

Fear may protect us from loss, pain, or death, but we know that in many ways it can cause us to be more vulnerable to all three as well. And it can certainly stall and forestall gain.

It’s not the big public powerful builders who are suppressing recovery, or who are “unwilling” to risk building for people who can afford only $200,000 or $250,000 on their homes, as opposed to $300,000 or $400,000.

It’s the entire ecosystem that broke and decided that half of the people and half of the companies in the new residential construction business had to go that we’re up against in the new home supply vs. demand crunch.

Rose Quint, I think accurately, says it’s going to be start-ups, new home building companies who can make a go of it in today’s environment where land costs are not depressed, where home buyers are as discriminating as ever, and where a AD&C loan or a home loan is not a slam-dunk, who will be the make-or-break, not just of NAHB membership, but of our economy’s ability to continue clawing it’s way back above water.

When we can, at BUILDER, we’re going to start focusing on start-ups.

One thing is certain.

Builders don’t grow on trees.