The year’s most ambitious strategic combination and biggest transaction in home building–merging Ryland and Standard Pacific into the No. 4-ranked, $5.2-billion, newly named CalAtlantic–has officially made it across the legal, regulatory, organizational, and financial finish line.

The deal–first announced June 15 as a “merger of equals”–creates a 41-market, 17 state land empire and marketing and merchandising operation, whose market cap on June 30 rang in at $5.4 billion and whose enterprise valuation totaled $8.4 billion.

“We got it done on our planned time-table. Rarely does a merger of this size happen so fast,” said CalAtlantic president and chief executive officer Larry Nicholson, who spoke with BUILDER as the deal closed. “We came to realize that we were more even more alike as companies than we originally anticipated.”

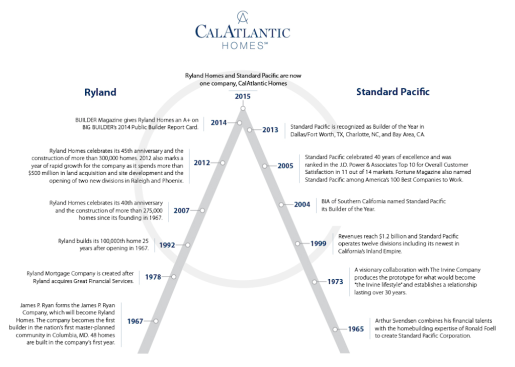

In contrast with a couple of the era’s other “mega-mergers”–Pulte’s $1.4 billion stock purchase of Centex in the Summer of 2009, and TRI Pointe’s more recent $2.8 billion acquisition of the Weyerhaeuser portfolio of five private regional home building companies in June 2014–Standard Pacific and Ryland are choosing to submerge their respective 50-year-old former brand names for a newly chosen one, CalAtlantic.

“Management of both organizations agreed on a one-brand strategy from the start,” said Nicholson. “The name CalAtlantic is symbolic both of where we do business and the roots of our respective organizations, and it conveys the breadth and scope of our new national footprint.” Nicholson said that he and parts of the new CalAtlantic executive organization will establish a D.C.-area headquarters presence, while keeping a corporate presence in the Southern California area as well.

Communities and neighborhoods that have progressed beyond their build- and sell-out points will continue to go-to-market under the respective Ryland and Standard Pacific names, but new communities, and tracts that may have more than 24 months of selling horizon ahead of them will start to market under the new CalAtlantic aegis as early as January 2016.

“We have a lot of work ahead of us,” said Nicholson. “But the biggest challenges of the integration process are now behind us. It’s a new day for the company.” The new company will trade on the New York Stock Exchange as CAA.

Since the June announcement, Ryland and Standard Pacific executives have been working through an intensive operational integration sprint across their national footprint, re-organizing divisions to play to their new-found mult-tiered proficiencies from entry-level to just-shy of custom-style luxury. Their efforts will result in a first-wave reduction in the combined employee base of about 10%, according to Nicholson. Company reports say that “production, purchasing and other synergies from the transaction could result in annual cost savings of between $50-$70 million,” savings that can come of integrating operations in nine “overlap” divisions, as well as StanPac’s and Ryland’s respective mortgage companies.

With 76,000 owned- and controlled homesites, this single enterprise has land positions to suit customer segments considered to be the juggernauts of future new-home purchase growth–retiring Baby Boom adults with discretionary means to buy their “active adult” lifestyle dream home, and young adult “Millennials,” who are gaining traction in their careers after a slow start in the teeth of the Great Recession.

Aside from the product-line diversity, the deal gives CalAtlantic operational presence in 20 of the top 25 MSAs for new home construction, top-five status in 15 out of 20 of those markets. This market share strength and scale can work to the new organization’s benefit in relationships with trade subcontractor crews, who are in such scarce supply in many active home building markets, and with land-sellers, who may gravitate toward organizations with a consistent appetite for lots across multiple customer segments through boom times and lean stretches in the market.

Not to be ignored in the mix of strategic and operational goals, the cost of borrowed money in the public debt markets may drop as the combined entities achieve financial “synergies” and improve their credit rating profile.

Now that the two companies have submerged legacy, ego, and operational style differences into a single entity, it will be fascinating to observe whether the combination can leap-frog into competition with the holy trinity of home builders, D.R. Horton, Lennar, and Pulte, who play at another level higher than the rest of the 100 top companies.

Depending on how effectively and efficiently CalAtlantic taps into, leverages, and builds value into its 76,000-lot empire, it could potentially give the Big Three a run for their money.

We believe that during the current recovery cycle–with its uncertainties, and fits-and-starts character–motivation for further consolidation remains, especially at the capital investment level. Fewer, larger operating entities make for a simpler, more straightforward investment analysis and decision-making.

There are still a fair number of strong players in strong markets that are being courted by large, potential acquirers, and being smaller means having less clout and tougher access to growth capital even as bank lenders say they’ve opened their purse-strings.

So, more big deals are likely, and many more smaller deals are inevitable in the months ahead, particularly as technology and management processes begin to offset the complexities of local real estate and local job site issues.