For Jerry Wade, president of Artistic Homes in New Mexico, dealing with banks these days is the stuff of nightmares. “You just want to tell them they can go kiss the south end of an elephant going north,” he says.

The problems started when the bank he’d dealt with for more than 20 years joined the ranks of the more than 200 banks the Federal Deposit Insurance Corp. has taken over since the sub-prime mortgage crisis sent the American financial industry into a tailspin. Since then, he’s been looking for a new source of financing—with little luck.

He says it’s hardly worth hitting up other banks, as he knows “a lot of builders who can’t build a damn pre-sold home.” The banks have little appetite for vertical financing and even less for horizontal. For the moment, he gets by thanks to a private investor who has been buying land for him.

“In 1984, ’85, things were bad,” Wade says. “But it’s nothing like what we’ve got going on now. It’s just ridiculous.”

Wade’s grumblings are a common refrain among the private builder set these days. For as much as private builder executives are business managers, many of them are also business owners who’ve poured their hearts, souls, and savings into growing their business in the best of times and keeping them alive in the worst of times—of which the past three years most definitely qualify.

However, patches of blue have begun to appear in what’s otherwise a dark and cloudy sky for home building. New-home demand has a pulse again, home prices have stabilized, and land remains a bargain. Normally, those are signals that it’s time, after years of atrophy, to begin to rebuild a future, one where success means more than just keeping the lights on.

But the banks aren’t biting. In fact, they continue to pull back on lending in the sector, further curbing their exposure to the home building industry until asset valuations find a firmer floor. According to information from Zelman & Associates, banks reduced acquisition, development, and construction (AD&C) lending by 23 percent last year and are on track to pare that down another 26 percent in 2010.

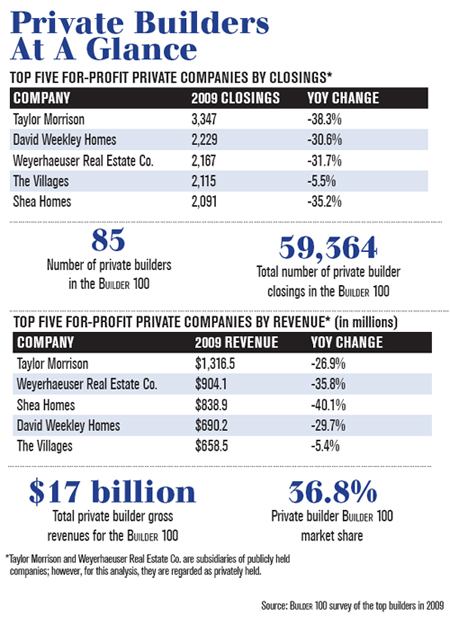

Still, many privates have to replenish community counts to spark cash flow from sales; others need to access lower-priced land to balance their portfolios and rebuild profitability. Without access to capital, many private builders are finding not only their recovery but their survival once again threatened.

“The recovery has started, and if we can’t build homes, why did we tough it out?” asks John Wieland, founder of namesake John Wieland Homes & Neighborhoods. “Why did I put all this personal money into the company? The answer is, I did it to get to the upturn, and now, if we can’t enjoy the upturn, it looks like I made a big mistake.”

PUBLIC OPTIONS At the same time that private builders find themselves manacled by capital constraints, their public builder counterparts are having few of the same issues.

Collectively, the publics raked in roughly $2 billion in tax refunds from Congress’ extension of the net operating loss tax carryback provision. Moreover, the publics have successfully tapped the public markets, raising additional equity and buying back debt for premiums of cents on the dollar.

And without the encumbrances of financing provisions like secured debt, personal guarantees, subdivision bonds, and the like, public builders are becoming tougher competition for the private guys. “The current situation is giving public builders tremendous advantage and market share,” says Bill Hoover, who leads operations for Las Vegas-based Adaven Homes.

And the publics are hardly being shy when it comes to deploying those capital resources. In fact, many are aggressively pursuing finished-lot land deals and are reported to be gobbling up lots as fast as banks can spit them out through the REO process. This feeding frenzy, which is going far in recalibrating land values, also is beginning to drive prices north.

“The publics pay 2.5 times what we’d pay,” says Scott Shapiro, CFO for Florida-based Highland Homes. “I don’t know how they are doing it … but they can do it because they pay cash.”

What’s left for private builders are carrion—20-lot deals, scattered lots, and other “screwball lots,” says Hoover. “You can’t build a business on that,” he says.

LOTS NEEDED Privates have had to dig deep, get creative, and turn to relationships for an edge. Land owners and developers sometimes accommodate this group’s constraints, signing over lots to builders but agreeing to wait for payment until the homes built on the lots are closed.

Similarly, bank fee-building deals allow private builders to build without paying for lots. But for as much as the fee structure means revenue, it’s not a sustainable business model. It might temporarily serve to pay their bills, but there’s not much left after overhead.

So, sweetheart developer deals and fee-building only go so far. Firms need not only to reload with lower-priced land but also do so with enough scale to capture efficiencies if they plan to partake in the next up cycle.

It’s hard to see how. Despite fears over the future of community banks, a few financially surefooted ones are stepping up to fill the financing void left by big commercial banks. Builders are going to see higher rates on the capital—prime-plus versus LIBOR-plus—but many see it as the last best option.

Of course, making that option a reality is easier said than done.